http://www.reuters.com/article/2011/...7BL0MC20111222The federal government, as has been widely noted, has pressed few criminal cases against major lenders or senior executives for the events that led to the meltdown of 2007. Finding hard evidence has proved difficult, the Justice Department has said.

The government also hasn't brought any prosecutions for dubious foreclosure practices deployed since 2007 by big banks and other mortgage-servicing companies.

But this part of the financial system, a Reuters examination shows, is filled with potential leads.

Foreclosure-related case files in just one New York federal bankruptcy court, for example, hold at least a dozen mortgage do ents known as promissory notes bearing evidence of recently forged signatures and illegal alterations, according to a judge's rulings and records reviewed by Reuters. Similarly altered notes have appeared in courts around the country.

Banks in the past two years have foreclosed on the houses of thousands of active-duty U.S. soldiers who are legally eligible to have foreclosures halted. Refusing to grant foreclosure stays is a misdemeanor under federal law.

The U.S. Treasury confirmed in November that it is conducting a civil investigation of 4,500 such foreclosures. Attorneys representing service members estimate banks have foreclosed on up to 30,000 military personnel in potential violation of the law.

In Alabama, a federal bankruptcy judge ruled last month that Wells Fargo & Co. had filed at least 630 sworn affidavits containing false "facts," including claims that homeowners were in arrears for amounts not yet due.

Wells Fargo "took the law into its own hands" and disregarded laws banning perjury, Judge Margaret A. Mahoney declared.

And in thousands of cases, do ents required to transfer ownership of mortgages have been falsified. Lacking originals needed to foreclose, mortgage servicers drew up new ones, falsely signed by their own staff as employees of the original lenders - many of which no longer exist.

But the mortgage-foreclosure mess has yet to yield any federal prosecution against the big banks that are the major servicers of home loans.

Last edited by Winehole23; 12-27-2011 at 12:24 PM. Reason: link edited. works for me.

link @ reuters, aboveBanks in the past two years have foreclosed on the houses of thousands of active-duty U.S. soldiers who are legally eligible to have foreclosures halted. Refusing to grant foreclosure stays is a misdemeanor under federal law.

The U.S. Treasury confirmed in November that it is conducting a civil investigation of 4,500 such foreclosures. Attorneys representing service members estimate banks have foreclosed on up to 30,000 military personnel in potential violation of the law.

Last edited by Winehole23; 12-27-2011 at 12:19 PM.

sameIn Alabama, a federal bankruptcy judge ruled last month that Wells Fargo & Co. had filed at least 630 sworn affidavits containing false "facts," including claims that homeowners were in arrears for amounts not yet due.

however, inasmuch as prosecution impedes the rate of clearance, it is considered bad medicine, like all that does not serve the utmost expedience of business

the good of letting all the fraudulent paper pass as good outweighs the legal accountability of fraudsters, or restoring adherence to law. in fact a thorough legal accounting could be injurious to our economic well-being, well-placed and reliable sources say...

multi-state settlement could leave investors holding the bag:

http://www.ft.com/intl/cms/s/0/ae955...#ixzz1iesnyXnP

LPS on Mortgages: "Trend toward fewer loans becoming delinquent has halted"

The November Mortgage Monitor report released by Lender Processing Services, Inc. shows that while mortgage delinquencies at the end of November 2011 were nearly 25 percent less than the January 2010 peak, the trend toward fewer loans becoming delinquent, which dominated 2010 and the first quarter of 2011, appears to have halted. At the same time, new problem loans – those loans seriously delinquent as of the end of November that were current six months prior – have not improved significantly in the last year. This degree of stagnation indicates that while the situation is not getting markedly worse, it is not improving either, and inventories of troubled loans remain significantly higher than pre-crisis levels across the board.

http://www.calculatedriskblog.com/20...ard-fewer.html

Details of Mortgage Servicing Settlement Between Banks and AGs Begin to Emerge

The big number is the $25 billion that the banks will commit to three categories of the settlement: $5 billion in cash payments, mostly to the states, $3 billion in refinancing for underwater mortgages, and $17 billion in principal reduction. Here’s the breakdown:

http://swampland.time.com/2011/12/23...ag-banks-deal/

===

No doubt that the banks will "settle" for a handslap. $25B is chump change compared to the profits they made and the taxpayer bailout, even chump change compared to the executive bonuses.

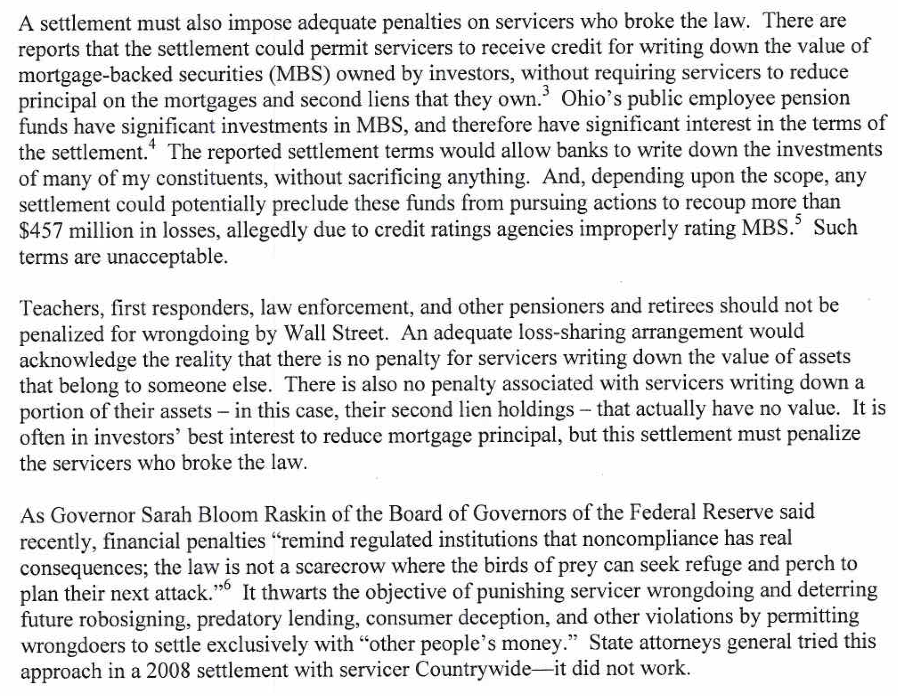

http://www.bloomberg.com/news/2012-0...skin-says.htmlFederal Reserve Governor Sarah Bloom Raskin said the central bank should fine mortgage servicing companies that broke the law and are partly to blame for the current “foreclosure crisis” in U.S. housing.

“The Federal Reserve (FDTR) and other federal regulators must impose penalties for deficiencies that resulted in unsafe and unsound practices or violations of federal law,” Raskin said in a speech today in Washington. “The Federal Reserve believes monetary sanctions in these cases are appropriate and plans to announce monetary penalties,” she said.

The Fed in April initiated formal enforcement actions against 10 banking organizations to address a “pattern of misconduct and negligence” in mortgage loan servicing and foreclosure processing.

“One purpose of monetary penalties, when they are appropriately sized, is to incentivize mortgage servicers to incorporate strong programs to comply with laws when they build their business models,” Raskin said. “This is an operational purpose, but as mentioned earlier, monetary penalties also remind regulated ins utions that non-compliance has real consequences.”

The 10 ins utions the Fed announced enforcement actions against included Bank of America Corp. (BAC), Citigroup Inc. (C), Ally Financial Inc., HSBC North America Holdings, Inc., JPMorgan Chase & Co. (JPM), MetLife, Inc., PNC Financial Services Group, Inc., SunTrust Banks, Inc., U.S. Bancorp, and Wells Fargo & Co.

New York Investigates Forced-Place Insurance Scams

The investigation centers on so-called force-placed insurance that has become increasingly common since the downturn of the housing market began and homeowners had trouble keeping up with payments on their home insurance.

JPMorgan Chase, Bank of America, Citigroup and Wells Fargo are among the major companies involved in the inquiry by the office of Benjamin M. Lawsky, the superintendent of New York States Department of Financial Services, according to a person briefed on the investigation who asked to remain unidentified because the matter was private.

Mr. Lawskys office issued 31 subpoenas or other legal notices related to the case in early October, just as the states insurance and banking departments were merged under his new agency. His office has already turned up instances where mortgage servicing units at large banks steered distressed homeowners into insurance policies up to 10 times as costly as the homeowners original plans.

In some cases, those policies were offered by affiliates of the banks themselves, raising questions about conflicts of interest; in other cases, there may have been kickbacks between unrelated companies, according to the person briefed on the investigation.

Dodd-Frank made this type of forced-place insurance scam illegal. Yet, despite the fact that weve known about this for years, it takes the New York State Department of Financial Services to run the investigation. Presumably the Consumer Financial Protection Bureau, now newly bolstered with the ability to regulate non-bank financial operations like mortgage servicers, can get involved. But Dodd-Frank makes it unclear who is supposed to regulate forced-place insurance scams at the federal level. Until then, we have to rely on the states.

, they also found the exact same robo-signing problem weve seen in foreclosure fraud:

In April of last year, Chase ceased filing claims altogether in Dade County. That month, The Wall Street Journal first reported that Chase had dropped more than a thousand consumer debt cases around the country. Some contract attorneys cited do entation irregularities for the move, the paper reported.

Robo-signing, or the high-volume production of signed legal do ents, has been a key element of the governmental and media foreclosure reviews. Chases current pullback raises at least the possibility that at least some banks may have do entation problems in other business lines.

Any deal made with banks on their crimes simply perpetuates an industry that mostly profits off those crimes.

http://news.firedoglake.com/2012/01/...surance-scams/

I assume the entire financial sector is one big criminal fraud, a house of cards, a Wizard of Oz, until proven otherwise. But it's so powerful, it's effectively immune from policing and prosecution, beyond a couple token cases.

Last edited by boutons_deux; 01-14-2012 at 04:20 PM.

Occupy the Neighborhood: How Counties Can Use Land Banks and Eminent Domain

An electronic database called MERS (Mortgage Electronic Registration Systems) has created defects in the chain of le to over half the homes in America. Counties have been cheated out of millions of dollars in recording fees, and their le records are in hopeless disarray. Meanwhile, foreclosed and abandoned homes are blighting neighborhoods. Straightening out the records and restoring the homes to occupancy is clearly in the public interest, and the burden is on local government to do it. But how? New legal developments are presenting some innovative alternatives.

http://www.truth-out.org/occupy-neighborhood/1326472096

Foreclosure-to-Rental Screwjob

“The paper also signaled that the Fed…. will try to involve banks more directly in housing-revival approaches… One area involves efforts to turn foreclosed homes into rental properties….

Banking regulations typically direct banks to sell foreclosed homes quickly, although the rules do recognize this isn’t always practical and so these properties can be held up to five years. The Fed said it is now “contemplating issuing guidance” to banks and regulators that would possibly allow banks to turn some of these foreclosed homes into rental properties…..The hope is this may help stanch the flow of foreclosed properties into markets…” (“Fed Up With the Depressed State of Housing”, Wall Street Journal)

Bingo. The banks are not only sitting on 1.7 million shadow inventory of homes they’ve stockpiled to keep prices artificially high. They also have millions more in the pipeline when a settlement is finally reached on the robo-signing scandal. So, what are they going to do with all that backlog?

That’s easy. They’ll schluff it off on the taxpayer by creating a foreclosure-to-rental swindle where the government provides lavish incentives for banks and private equity scavengers to buy the homes (in bulk) for pennies on the dollar with loans provided by–you guessed it–Uncle Sam. Here’s a summary of what’s going on behind the scenes:

“As the Obama administration and federal regulators work on a program to sell government-owned foreclosures in bulk to investors, those investors aren’t wasting any time stockpiling cash and buying foreclosed properties at auction and from the major banks.

Oakland, California-based Waypoint Real Estate Group, a major acquirer of so-called “REO to Rental” (Real Estate Owned) just announced a partnership with a private equity firm, Menlo Park, California-based GI Partners, to buy foreclosed properties….

“Our approach to buying distressed single-family houses, renovating them, and leasing to residents who are committed to a path to future home ownership is a viable solution to our nation’s housing crisis,” said Colin Wiel, managing director and co-founder of Waypoint in a press release. “Our partnership with GI Partners ensures we can take the next step in our company’s evolution.”

GI is taking an increasingly popular bet on distressed real estate, closing on a $400 million fund with Waypoint, which has plans to purchase $1 billion in distressed real estate assets over the next two years, according to its release. (“Private Equity Readying a Run on Foreclosures”, Diana Olick, CNBC)

So, what do these guys know that we don’t know? And why are they plunking down big money when the details have not even been released yet?

None of this really passes the smell test, does it? The only thing we know for sure is that the “fix is in” and that Bernanke will do what he always does when the banks are in a pinch. Throw them a lifeline.

http://www.counterpunch.org/2012/01/...ntal-screwjob/

One of Barry's major re-election comments: "the banks didn't do anything illegal"

The financial sectors OWNS the federal govt.

"Here's some pocket change, we keep the houses, and we promise not to do it again"

http://mobile.sfgate.com/sfchron/db_...l=true#display

Thanks NC Readers! Tom Miller Says No Mortgage Deal Imminent

Readers no doubt saw both on this site and elsewhere that the Obama Administration was cranking the heat up on the mortgage settlements talks, and was apparently planning to go ahead with the Federal regulators inking a pact, on the assumption they’d get enough state attorneys general to provide at least a modest fig leaf. The assumption also seemed to be that the Administration could enlist Congressmen to pressure some of the current and rumored dissident Democrat AGs to fold and join the Obama camp.

That effort appears to have gotten such a large repudiation today, when the settlement terms were presented in Chicago to Democratic AGs and discussed over the phone with the Republican AGs that Tom Miller who is leading the attorney general negotiations has done a major climbdown:

FOR IMMEDIATE RELEASE

January 23, 2012

STATEMENT FROM ATTORNEY GENERAL TOM MILLER

(CHICAGO, Illinois) State Attorneys General from both parties, along with our federal partners, are today discussing the details of the progress we have made so far in settlement negotiations, including the terms we must still resolve. We have not yet reached an agreement with the nation’s five largest servicers, and we won’t reach a settlement any time this week.

What is intriguing here is the Miller camp claim (effectively) that there never had been a deal on the table. That contradicts the story in the Financial Times last week and a report I had gotten from an investor with good contacts on the Republican side. Since Miller has repeatedly played fast and loose with the truth, I’m not sure I believe the message implied here, that they are still moving forward on a deal, just more slowly than they had messaged, as opposed to a deal on the table came unglued and they need to regroup in a more serious way.

We will hopefully get more intelligence (or maybe just better attempts at disinformation) but I read this as an indication the deal agreed between the Federal regulators and the biggest servicers somehow came unglued. Possibilities include: someone exposed a definitional/drafting flaw (the Feds thought it meant one thing and the banks thought it meant another); someone (one of the banks?) retraded the deal; the Administration has assumed it could rely on a certain minimum number of AGs to fall in line and they regarded that minimum number as essential, and the pow wow today exposed that they are below that level.

Regardless, this is positive news, since it vindicates the courageous attorneys general who are pressing forward with investigations and prosecutions rather than trying to cover up pervasive fraud by servicers. Thanks so much to NC readers for your calls to attorneys general. You helped play a role in telling the Administration that the public will not support coverups when enforcement and reform are what is really needed.

http://www.nakedcapitalism.com/2012/...+capitalism%29

http://readersupportednews.org/opini...ulism-for-realhere is a lot to digest in a recent series of events on the Prosecuting Wall Street front - the two biggest being Barack Obama's decision to make New York Attorney General Eric Schneiderman the co-chair of a committee to investigate mortgage and securitization fraud, and the numerous rumors and leaks about an impending close to the foreclosure settlement saga.

There is already a great debate afoot about the meaning of these two news stories, which surely are related in some form or another. Some observers worry that Schneiderman, who over the summer was building a rep as the Eliot Ness of the Wall Street fraud era, has sold out and is abandoning his hard-line stance on foreclosure in return for a splashy federal posting.

Others looked at his appointment in conjunction with other recent developments - like the news that Tim Geithner won't be kept on and Obama's comments about a millionaire's tax - and concluded that Barack Obama had finally gotten religion and decided to go after our corruption problem in earnest.

At the very least, Obama's recent acts were interpreted as a public move toward economic populism: if the president was looking to associate himself with that word, he did a good job, since there were literally hundreds of headlines about Obama's "populism" the day after his State of the Union speech.

I think it's impossible to know what any of this means yet. There is a lot to sort out and a lot that will bear watching in the near future.

Sundering the Social Contract

there is a new battleground in what’s known as the housing market with as many as 14 million Americans in or facing foreclosure.

Jean-Jacques Rousseau

The defense of property rights is the holy of the holies for the propertied classes with a whole industry set up to enforce their claims of ownership.

We have seen how this plays out with the courts, run by often bought-off and complicit judges rubber-stamping claims by banks and realty interests even when laws are disregarded amidst fraudulent filings, biased contracts, and phony robot signings.

They control the marshals who seize your property and they constantly denigrate the real victims as “irresponsible.” It’s not surprising any more to read about banks foreclosing on properties they don’t even own.

“The concept is that man standing alone is more vulnerable than many men united each in defense of the other. This condition makes it impossible for one to hurt an individual without hurting the whole group or for one to hurt the group without affecting each individual.

“There is now a social contract where individual rights are combined. In this case, it is in the best interest of the individual to give over his rights to the group since he has a more powerful protective base than standing alone.”

And yet many of us today do “stand alone:” in the commercial marketplace where borrowers are seen as suckers by lenders and fraud is pervasive. Abuse, lying and theft are built into the equation.

“During the Savings and Loan crisis, Bill Black reminds us that there were about a thousand FBI agents working on the various cases. That’s one hundred times the number of people working on a scandal that is about forty times larger and far more complex.

“To put it another way, let’s say that this scandal cost the American public $5-7 trillion in lost home equity. That’s about $100 billion of lost home equity per person assigned to this task force. If someone stole $100 billion a corporation, like say, if somehow Apple’s entire cash hoard which is roughly that amount, suddenly disappeared, I’m guessing that the FBI would assign more than one person to the case

“There are two underlying structural problems with the new(ish) Federal task force on financial fraud,” he writes. “One, it is the policy of the administration to protect the banking system’s basic architecture, which means the compensation structure and the existing personnel who run these large ins utions.

“Any real investigation into the financial collapse will inevitably lead to the collapse of this architecture. Thus, any real investigation will be impeded when it begins to conflict the basic policy framework of the Obama administration. And this framework is set by Obama. It’s what he believes in. He made this clear in his first State of the Union, when he said a priority of the administration was to ensure that ‘the major banks that Americans depend on have enough confidence and enough money to lend even in more difficult times.’”

Perhaps this is why so few bankers have spoken out loudly about this latest effort to target their financial frauds. They know it’s not serious and recognize that political business, like the news business, is now a branch of show business.

http://consortiumnews.com/2012/01/28...cial-contract/

http://www.ft.com/intl/cms/s/0/53ec3...#axzz1kadWIzO5A federal auditor has warned that the Obama administration’s failure to crack down on recalcitrant banks risks harming distressed borrowers.

The warning, offered in a report released early Thursday, contrasts with comments earlier in the week by Barack Obama, US president, who chided banks for giving borrowers the “runaround” when it came to lowering their mortgage payments through refinancings.

The US Treasury department has the authority to penalise banks for their noncompliance with the administration’s Making Home Affordable programme, but it has not been using that authority to ensure banks are not harming homeowners and improperly benefiting from taxpayer-provided aid, according to the Special Inspector General for the Troubled asset relief programme (Sigtarp).

The audit underscores the degree to which, three years after coming into office, Mr Obama has fallen short on promises to help troubled borrowers keep their homes. Initiatives launched beginning in early 2009 have fizzled out, disappointing members of Congress, key administration officials and Mr Obama’s supporters.

There are currently 1 users browsing this thread. (0 members and 1 guests)

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote

http://brown.senate.gov/imo/media/doc/011912%20AG%20Settlement%20Letter.pdf

http://brown.senate.gov/imo/media/doc/011912%20AG%20Settlement%20Letter.pdf