Reply With Quote

Reply With Quote

Ignores the pandemic induced supply shock, but the greedflation hypothesis has legs imo.

https://heisenbergreport.com/2023/03...-greedflation/

Musk wanted then to lower the rate

That would have been better

Fools

Ignores the pandemic induced supply shock, but the greedflation hypothesis has legs imo.

https://heisenbergreport.com/2023/03...-greedflation/

Fed started posting weekly losses last September, this week it has reached operating losses of ~$40b.The reason why is the same asst liability-maturity mismatch that sunk SVB. Technically, the losses are booked as deferred assets and don't affect the Fed's ongoing operations, but Fed remittances (~$100b a year) to the US Treasury will cease until the shortfall is made up for.

It's the first operating loss in the Fed's history

Political pressure will be applied to monetary policy.

I posted an article about a taper tantrum that didn't happen in 2016 because it has no contemporary political axe to grind, most of the articles I could find that came out this week do. AEI dudes, Mises Ins ute flacks, crypto bros, goldbugs and Catholic fascists.

https://www.businessinsider.com/wall...tantrum-2016-9The crisis comes when Congress realizes the Fed is paying the government nothing (or next to nothing) while s ing out billions to the banks. Several members of Congress have already been critical of Fed payments to banks, but theyve largely missed the mark. When the next budget crisis arises without the Fed paying its perceived fair share, all it would take is a few impassioned speeches to stir the masses and make monetary policy a de facto political animal.

The worst possible outcome would be for a fickle and indecisive Congress to assert its authority over monetary policy. Unfortunately, by waiting seven years to raise ratesand into an economy growing at best modestlythe Fed has backed itself into a corner. The Fed has clearly chosen the banks over the best interests of the taxpayers, and this will eventually come back to bite Chair Yellen.

Fed started posting weekly losses last September, this week it has reached operating losses of ~$40b.The reason why is the same asset liability-maturity mismatch that sunk SVB. Technically, the losses are booked as deferred assets and don't affect the Fed's ongoing operations, but Fed remittances (~$100b a year) to the US Treasury will cease until the shortfall is made up for.

It's the first operating loss in the Fed's history

Political pressure will be applied to monetary policy.

I posted an article about a taper tantrum over rate hikes that didn't happen in 2016 because it has no contemporary political axe to grind, most of the articles I could find that came out this week do. AEI dudes, Mises Ins ute flacks, crypto bros, goldbugs and Catholic fascists.

https://www.businessinsider.com/wall...tantrum-2016-9The crisis comes when Congress realizes the Fed is paying the government nothing (or next to nothing) while s ing out billions to the banks. Several members of Congress have already been critical of Fed payments to banks, but theyve largely missed the mark. When the next budget crisis arises without the Fed paying its perceived fair share, all it would take is a few impassioned speeches to stir the masses and make monetary policy a de facto political animal.

The worst possible outcome would be for a fickle and indecisive Congress to assert its authority over monetary policy. Unfortunately, by waiting seven years to raise ratesand into an economy growing at best modestlythe Fed has backed itself into a corner. The Fed has clearly chosen the banks over the best interests of the taxpayers, and this will eventually come back to bite Chair Yellen.

Red diaper babies at WSJ

the commies at Business Insider

https://www.businessinsider.com/why-...es-jobs-2023-4But a new paper from the University of Massachusetts Amherst economists Isabella Weber and Evan Wasner argues that our current bout of inflation is what they call sellers' inflation. Bottlenecks like those rampant supply-chain shortages give firms what the economists call "temporary monopoly" status. Compe ion between firms in the industry, as well as the possibility of new companies trying to edge in on their territory, dwindles. And because many of these industries are so concentrated, with just a handful of companies dominating the market in any given area, it's easier for firms to reach an implicit agreement that, yes, they're all going to raise their prices.

Companies that don't fall in line and try to undercut their rivals to attract deal-conscious customers face discipline for not following the status quo. Wasner and Weber use the examples of Target and Walmart, which both tried to weather some costs without raising prices in an attempt to hold onto customer loyalty. This effort to keep prices low was greeted with disdain. Investors saw the price-hike-driven profits being made by compe ors and sold off their Walmart and Target stock, in effect "penalizing their pricing strategy," according to Wasner and Weber.

Researchers at the Federal Reserve Bank of Boston similarly found in a 2022 study of inflation patterns that monopolistic concentrations in some sectors made price increases worse than they had to be. If there's no one challenging you with better deals or cheaper goods, you have free rein to hike prices as you wish.

we've been doing this for 14 years, basically paying banks tens of billions of dollars a year to sit on their treasure hoard, doing nothing with it.

https://cepr.org/voxeu/columns/extra...ons-its-originOne legacy of quan ative easing (QE) is that banks have ac ulated huge amounts of bank reserves. As a result, the bank reserves market is characterised by a large excess supply. This has kept the money market (interbank) rate stuck at the zero lower bound for many years, until the central banks felt compelled, from early 2022 on, to raise interest rates to fight inflation. Given the excess supply of bank reserves central banks could only perform this feat by raising the rate of remuneration of bank reserves. As a result, this rate of remuneration became the new (not zero) lower bound in the money market (De Grauwe and Ji 2023a, 2023b).

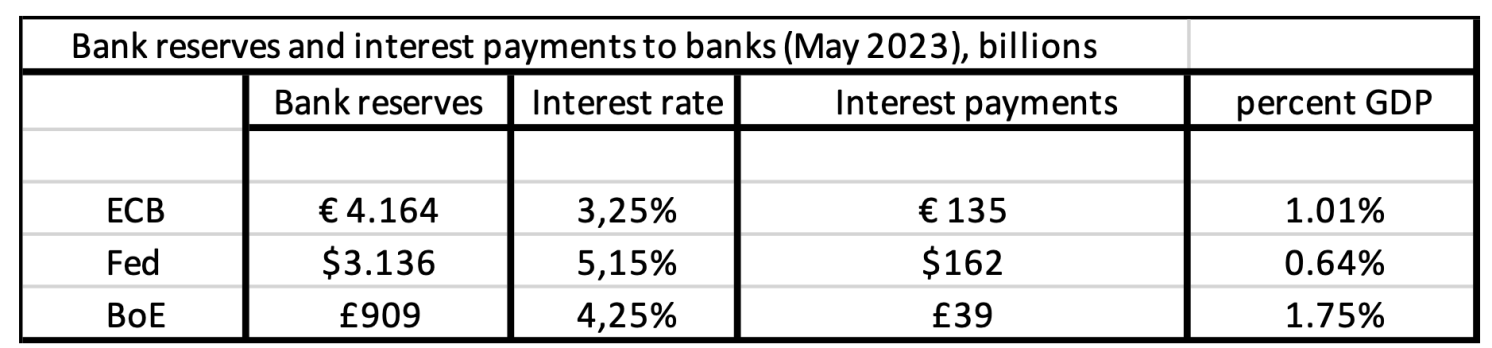

This policy now has created a lot of ‘collateral damage’. Since the stock of bank reserves is extremely high, the central banks now pay out large amounts of interest rate remunerations to banks, which increase with every interest rate hike. We show this in Table 1. This presents the outstanding bank reserves in the euro area, the US, and the UK in May 2023. We also show the interest rates prevailing at that time (second column). The third column presents the total interest payments made by the respective central banks to their domestic banks. The last column expresses these as a percent of GDP.

These are substantial numbers. To give some perspective, these interest payments exceed the seigniorage gains (profits) of modern central banks. For the US, for example, it has been estimated that seigniorage gains are less than 0.5% of GDP (Barro 1982, Cutsinger and Luther 2022). 1 Thus, as a result of their anti-inflationary policies, central banks transfer more than the total seigniorage gains to private banks. An extraordinary outcome of the fight against inflation. This is all the more spectacular as the seigniorage gains of central banks find their origin in the monopoly power granted by governments to central bankers. One would expect that these monopoly profits would then be returned to the government. Instead, they are returned more than fully to private agents.

Table 1

Source: De Grauwe and Ji (2023b), Board of Governors of the Federal Reserve, and ECB.

Fed remittances (~$100b a year) to the US Treasury will cease until the shortfall is made up for.

- The deal, orchestrated and backed by the Swiss government, was also much more costly than UBS initially bargained for, the filing showed.

- Over the course of the brief negotiations, the sum trebled from around $1.1 billion (1 billion Swiss francs) to roughly $3.3 billion (3 billion Swiss francs).

https://www.forbes.com/sites/roberth...suisse-rescue/

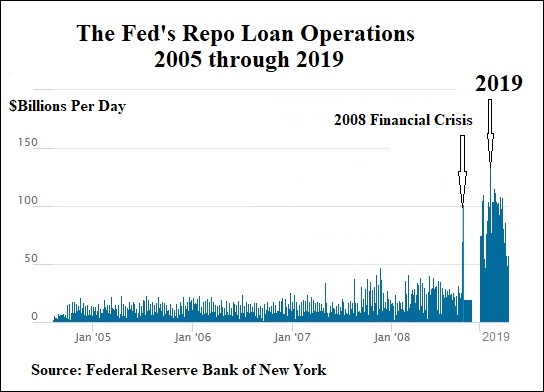

SOFR is the new LIBOR, FT sees a possible repeat of the 2019 "reverse repo ructions"

https://www.ft.com/content/b7597b71-...f-b6df6ad3c307

Indeed, Bank of Americas Mark Cabana estimates that this was the single-biggest SOFR e since Covid-19 wracked markets in early 2020, and points out it happened on record trading volumes.Cabana says he was initially too hasty in dismissing the e as driven by a short-term collateral shortage and unusually large amounts of window-dressing by banks. In a note published yesterday, he admits to overlooking something potentially more ominous: reserves seeping out of the banking system.

We have long believed funding markets are determined by 3 key fundamentals: cash, collateral, & dealer sheet capacity. We attributed last weeks funding e to the latter 2 factors. We overlooked extent of cash drain in contributing to the pressure.The increased sensitivity of cash to SOFR hints of LCLOR.LCLOR stands for lowest comfortable level of reserves, and might require a bit more explanation.

Back in ye olde times (pre 2008), the Fed set rates by managing the amount of reserves sloshing around the US monetary system. But since 2008 that has been impossible due to the amount of money pumped in through various quan ative easing programmes. That has forced the Fed to use new tools like interest on overnight reserves to manage rates in what economists call the abundant reserve regime.

But the Fed has now been engaging in reverse-QE or quan ative tightening by shrinking its balance sheet sharply since 2022.The goal is not to get the balance sheet back to pre-2008 levels. The US economy and financial system is far larger than it was then, and the new monetary tools have worked well.The Fed just wants to get from an abundant reserve regime to an ample or comfortable one. The problem is that no one really knows exactly when that happens.

As Cabana writes (with FT Alphavilles emphasis in bold below):Like the macro neutral rate, LCLOR is only observed near to or after it is reached. We have long believed LCLOR is around $3-3.25tn given (1) bank willingness to compete for large time deposits (2) reserve / GDP metrics. Recent funding vol supports this.A similar dynamic was seen in 19. At that time, the correlation of changes in reserves to SOFR-IORB turned similarly negative. The sensitivity of SOFR to reserves correlation signalled nearing LCLOR. We sense a similar dynamic is present today.

as to whether the president can fire the Chairman of the Fed, I think the answer is yes

https://x.com/RudyHavenstein/status/1858964507181412400

Trump with monetary clout would be an awesome power for good and for ill

Switzerland screwed bondholders, allegedly

https://www.ft.com/content/31801bcd-...6-b3087ab9627e

US asset manager AllianceBernstein is preparing to sue Switzerland for $225mn over the decision to wipe out $17bn of debt when the countrys government orchestrated the takeover of Credit Suisse by rival UBS last year.The group, which manages about $800bn in assets, is set to be added next month as a plaintiff in a case brought by law firm Quinn Emanuel Urquhart & Sullivan on behalf of Credit Suisse bondholders, according to people familiar with the details.AllianceBernstein will be the first large ins utional investor to join the claim and is expected to seek about $225mn in damages from the Swiss state, taking the total value of the lawsuit to $375mn, the people said.

The case, which was first filed in the Southern District of New York in June, relates to the writedown of Credit Suisses AT1 bonds when the scandal-hit lender was forced into a rescue merger with UBS in March last year.Quinn Emanuel has argued that the deal was brokered by the Swiss government and was an unlawful encroachment on investors property rights.AT1 bonds are a form of bank capital that converts into equity or is written down when a lender runs into trouble. However, the UBS Credit Suisse deal upended the traditional hierarchy among bank creditors by imposing losses on bondholders while allowing equity investors to recover $3.3bn.

I never heard a suitable explanation for this. Capitalism crushing traditional savers is a relative novelty.

one-month SOFR spread indicates liquidity tightening and market volatility

*US SOFR SURGED 18 BASIS POINTS TO 4.22%, MOST IN A YEARhttps://seekingalpha.com/article/483...ity-evaporates

- Market liquidity has dried up, with no immediate relief expected, leading to significant stress across risk assets and funding markets.

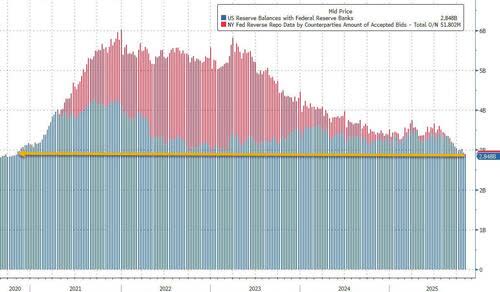

- The government shutdown pushed the Treasury General Account (TGA) above $1 trillion, draining Fed reserves and intensifying overnight funding pressures.

- Elevated SOFR and repo rates signal persistent volatility, with upcoming Treasury refunding announcements key to future liquidity direction.

- Low reserve balances and ongoing volatility suggest markets may face turbulence similar to late 2018, despite brief, limited relief ahead.

https://www.msn.com/en-ca/money/tops...ng/ar-AA1PIa2NThe one-month SOFR-fed funds futures spread is a key liquidity stress indicator: the more negative it is, the tighter repo funding conditions are perceived to be.

Following the Fed's policy decision this week, that spread hit minus 11.5 basis points (bps) for the November contract, a record gap. For December, the spread dropped to minus 12.5 bps, also an all-time low.

The numbers suggested that investors in the futures market expect SOFR to trade 11.5 bps and 12.5 bps higher, respectively, than the fed funds rate by the end of November and December.

(2018 was the worst year on Wall Street since 2008: https://www.cnbc.com/2018/12/31/stoc...ade-talks.html)

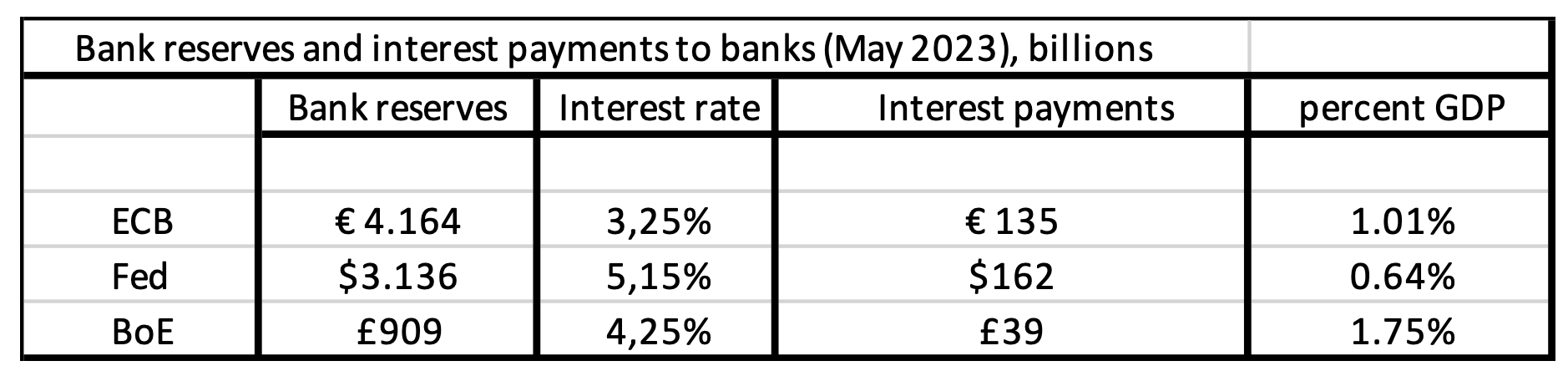

stealth QE to stem a liquidity crunch, like 2019

led to a melt up then, could be a bullish sign short term

could push valuations further away from fundamentals, worsening the inevitable correction

https://seekingalpha.com/article/484...bullish-signalIn September 2019, a critical but obscure part of the financial system broke. Overnight borrowing rates in the repo market suddenly ed from around 2% to over 10% in a matter of hours. Banks and dealers couldnt get the short-term funding they needed to finance Treasury holdings or settle trades. Liquidity froze. Wall Street was caught off guard. The Federal Reserve quickly intervened, launching emergency repo operations to inject cash into the system. Within days, funding markets stabilized. Over the next few months, the Fed expanded its balance sheet again, but not for QE, they insisted, but to keep repo markets functioning. That quiet intervention helped fuel the final leg of the markets rally into early 2020.

Currently, we are seeing cracks reemerge in this previously unknown part of the financial system. In todays commentary, we will discuss what it is and why it matters.

The repo market, short for repurchase agreement, sits at the heart of the financial system. Critically, and why it matters to the financial markets, is that it allows banks, hedge funds, and dealers to borrow cash by using high-quality securities, typically U.S. Treasuries, as collateral. (This is also how money winds up in the financial markets when the Federal Reserve is doing Quan ative Easing.)

The transaction is straightforward and is an overnight transaction. During this process, one party sells a security with a commitment to repurchase it the next day at a slightly higher price. That price difference represents the cost of borrowing. Typically, the difference between the Secured Overnight Financing Rate (SOFR) and the Interest Rate on Reserves (IOR) is slightly negative. Currently, that is not the case. Notably, this is not some niche corner of finance. Its the lifeblood of overnight funding.

Why is this so important? Because trillions flow through this market every day, and most people have never heard about it.

However, without it, Wall Street doesnt open.

- Dealers need it to fund their balance sheets.

- Hedge funds rely on it for leverage.

- Money market funds use it to park cash overnight.

- Its also how the Federal Reserve transmits monetary policy.

When the repo market functions smoothly, short-term interest rates stay in line with the Feds targets. When it breaks, liquidity dries up fast. That creates ripple effects in credit, equities, and even Treasury markets.

If repo transactions grind to a halt, its not because theres a lack of collateral or cash, but because of fear. When ins utions stop trusting each other, they stop lending to one another. Thats when the financial plumbing clogs, and the consequence of that clogged plumbing is rising volatility, strained liquidity, and falling asset prices. The repo market isnt just important. Its foundational.

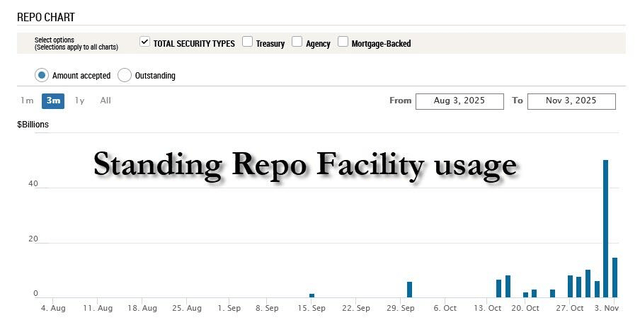

A Redux of 2019? What Does It Mean for the Markets?

Currently, cracks are reappearing. The overnight repo rate is climbing as the use of the Feds Standing Repo Facility is increasing, and treasury bill issuance is ballooning.

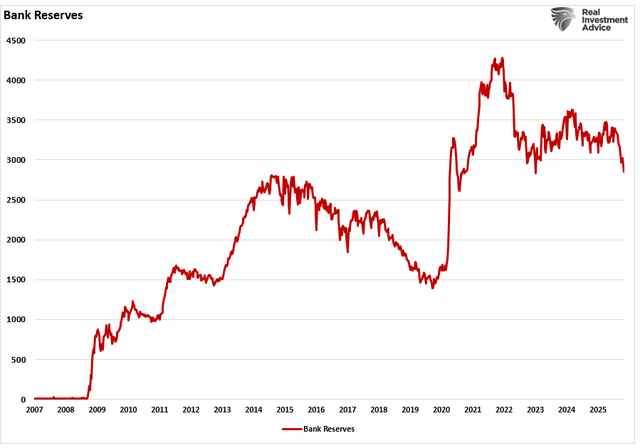

Most notably, what the Fed once deemed abundant liquidity has now fallen below the levels it considers ample. The chart shows that the Fed Reserves plus Reverse Repos (which, for the past three years, have served as an excess liquidity storage facility used primarily to fund purchases of T-Bills) is now at the lowest level since late 2020.

Sound familiar? It should. The current environment bears a striking resemblance to the lead-up to the September 2019 repo crisis. Back then, the repo rate suddenly ed from around 2% to over 10% in a single day as Wall Streets funding machine seized up. Here is an example of what happened.

You have a brand new, fully paid-for Mercedes. You go to your neighbor and ask for an overnight loan of just $10,000, offering him the le to your car as collateral. Your interest rate should be close to the Federal Reserves overnight rate, but instead, your neighbor says he wants 10%. That difference is a risk premium that is undeserved because the loan is backed by guaranteed collateral, in this case, the car.

But that is what happened in 2019, and the Fed had to intervene with emergency liquidity operations to restore stability.

Why did it happen? In 2019, a combination of tax payments and Treasury auctions drained reserves from the banking system. At the same time, dealers were loaded with collateral they couldnt finance. Cash lenders didnt want to step in, even at higher rates, because they were either constrained by regulation or unwilling to take the risk. The repo market, which had always been taken for granted, suddenly became the problem no one was watching.

Today, were seeing many of the same ingredients. Heavy Treasury issuance is forcing dealers to take on more collateral, and liquidity is being withdrawn from the system due to the Feds quan ative tightening. The problem with the repo market is why the Fed announced it would end the shrinkage of its balance sheet at the end of November. Meanwhile, bank reserve levels have dropped sharply, adding to concerns about overall liquidity.

When stress rises in the repo market, its not a technical glitch, but rather a signal that the financial system is under pressure. If this stress deepens, it could lead to a broad tightening of financial conditions that will spill over into the equity and credit markets. Given the Feds concern about the wealth effect the financial markets provide to economic growth, this has become the third, and unspoken, mandate of Fed policy.

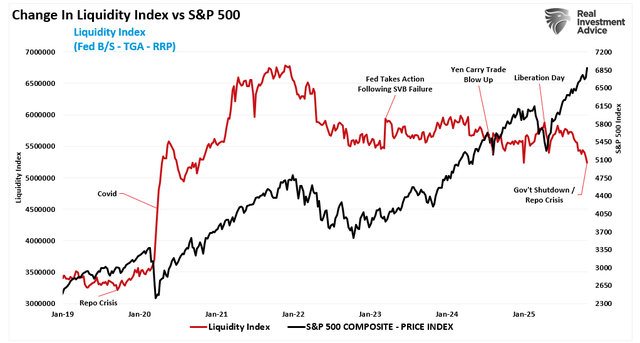

While that may sound frightening, there is a twist. If the Fed steps in to relieve repo pressure, like it did in 2019, it might trigger the opposite of a crash. In other words, the Feds actions to stabilize the repo market may lead to a melt-up in equities, where risk assets surge, not because fundamentals improve, but because liquidity returns in force. Such a conclusion is not far-fetched, as the Government shutdown has drained over $700 billion from the market, as shown by the sharp increase in the Treasury General Account.

Stealth QE on the Horizon

However, once the Government is reopened, that $700 billion increase in the Treasury General Account will flow back into the economy. That reopening will create a flood of effective stimulus as furloughed workers receive back pay, departments are reopened, and Government contract work resumes. Those dollars wind up deposited into the banking system, increasing bank liquidity. In effect, it is a stealth QE that could create a massive scramble for risk assets.

As such, both the end of the Government shutdown and a stabilization of the repo market could have an immediate impact on risk assets. Once dealers can fund collateral without paying punitive rates, liquidity will return, which greases the wheels of the entire financial system. Trading flows improve as Hedge funds can effectively re-leverage their portfolios, and credit spreads are expected to tighten.

You will notice in the chart below that this is precisely what happened after the 2019 repo scare. Once the Fed began daily operations to supply liquidity, the S&P 500 rallied to new highs. Then, of course, that liquidity went into overdrive following the onset of the pandemic. While it has since reversed somewhat, there remains, as noted above, ample liquidity in the financial system currently.

Just as it was in 2019, the move was not about fundamental improvements; it was simply about too much money chasing too few assets.

It is important to note that fixing the repo market isnt about bailing out Wall Street. Its about restoring the basic mechanics of financial intermediation. When overnight funding is cheap and available, ins utions are willing to trade, lend, and invest. That confidence feeds through to markets. Although most investors dont track repo rates daily, they feel the effects, as more liquidity means less volatility, tighter spreads, and rising asset prices. At least that is what we should expect in the short term.

However, the resolution needs to be more than a temporary patch. If the Fed signals its ready to backstop the market, investors will likely view that as a green light to increase equity risk and change the risk calculus to some degree. The problem is that stocks are already grossly detached from underlying fundamentals, and a resolution to either the Government shutdown or resolving the current repo stress will likely see investors pushing asset prices further away from those fundamentals. But that is how liquidity drives markets, especially when fundamentals look stretched.

For investors, it is worth noting that if the Fed steps in again, the upside could come quickly and substantially. For now, the repo market is the canary in the coal mine. What comes next depends on whether policymakers decide to move soon or wait until stress forces their hand.

Just bring back ZIRP for a year or so.

not gonna happen

that was an extreme measure to help us muddle through capitalism falling on its face in 2008

system of payment was imminently failing, so Obama saved the insolvent banks and nonbanks, the Fed ate the toxic derivatives and the American people ate

ZIRP was the muddle through, it lasted about a decade

The Fed can do reverse repo if the gubmint reopening injects too much liquidity

Trump will not allow the punch bowl to be taken away, most likely

who's your daddy?

Trump is your Daddy

he owns your ass for sure

There are currently 1 users browsing this thread. (0 members and 1 guests)

Posting Permissions

Posting Permissions