Reply With Quote

Reply With Quote

Meh. The federal government is now socializing basically any and all risk in the banking sector. Good business doesn't matter anymore.

Stupid business model. Gave rich tech guys stupid low interest mortgages on their megamillion dollar houses in exchange for them banking there. Zuckerberg got a 1% mortgage on like a 5+ million dollar loan.

Meh. The federal government is now socializing basically any and all risk in the banking sector. Good business doesn't matter anymore.

2nd largest bank failure in history, First Republic taken over by the regulator and sold to JP Morgan.

FDIC will share the losses in First Republic's loan book. Yet another "not a bailout" deal term the public will be on the hook for.

https://apnews.com/article/first-rep...3ac13e0a20955d

This is just starting. Banks vulnerable to commercial real estate loan will be next. I cut and pasted this from the first few paragraphs of a WSJ article today since it is subscription and won't let me link it.

A major Los Angeles office owner operated by Brookfield Asset Management is struggling to make mortgage payments as vacancies and rising interest rates disrupt the city’s commercial real-estate market.

The company, known as Brookfield DTLA Fund Office Trust Investor Inc., owns six Los Angeles office buildings and a retail center. Five of the office buildings face the risk of foreclosure, according to its public filings, and at least two of its mortgages are in default.

The company on April 21 filed to delist from the New York Stock Exchange after its market capitalization fell below $15 million. The company’s shares are down 87% since the start of the year to less than one dollar.

Brookfield DTLA’s troubles show how some bets on the office sector that held steady early on during the pandemic are starting to unravel amid rising vacancies and spiraling debt costs. The company is particularly vulnerable because the majority of its $2.3 billion in mortgages have floating interest rates and expire in 2023 or 2024.

Floating-rate loans, which often have shorter terms than fixed-rate mortgages, are emerging as flashpoints in a weakening office market. The cost of hedges that landlords buy to protect themselves against rising rates has surged, forcing them to either pay millions for a new hedge or default. When loans come due they are increasingly difficult to refinance because debt costs have risen, building values are down and many banks shy away from office mortgages.

Not a bailout, but a very sweet deal for JP Morgan

https://wolfstreet.com/2023/05/01/he...-of-investors/This is how JPM will benefit, according to JPM:

A one-time bargain purchase gain of $2.6 billion in 2023.

Over $500 million in annual net income accretion.

All producing an IRR (internal rate of return) of over 20%

.

Accelerates growth initiatives in JPMs U.S. wealth strategy.

Increased penetration with U.S. high net worth clients.

Adds prime locations in affluent markets (including San Francisco Bay Area, Los Angeles, Portland, Seattle, New York City, Boston, Jackson (Wyoming)

Accretive to tangible book value per share.

JPM bought assets it then wrote down to $184.7 billion:

$172.9 billion in loans at book value, which JPM wrote down 13% to $150.3 billion.

$29.6 billion in securities, which JPM continues to carry at par.

$5.0 billion in other assets, which JPM wrote down to $4.8 billion.

In addition, future credit losses on the loans (such as a result of foreclosure) are partially covered by a loss-share agreement. The FDIC will cover 80% of the losses from the single-family residential mortgages for seven years, and 80% of the losses of commercial loans, including commercial real estate (CRE) loans, for five years

Solution: put the public on the hook for 80% of the five year losses.

https://www.reuters.com/business/fin...al-2023-05-02/A key hurdle to doing a private sector deal, however, was that there were billions of dollars of unrealized losses on First Republic's books, and they would have to be funded if anyone bought the bank.

Is that surprising to you? The public is on the hook for everything.

Not surprised at all. Just laying out the deal terms.

TBTF

https://wallstreetonparade.com/2023/...ured-deposits/As of December 31, 2022, this is where deposits stood at the four largest banks in the U.S. all of which also have large risk exposure from their extensive trading operations on Wall Street: (The data comes from federal regulatory filings known as call reports.)

JPMorgan Chase Bank N.A. held $2.015 trillion in deposits in domestic offices, of which $1.058 trillion were uninsured.

Bank of America held $1.9 trillion in deposits in domestic offices, of which $909.26 billion were uninsured.

Wells Fargo held $1.4 trillion in deposits in domestic offices, of which $721.1 billion were uninsured.

Citibank N.A. (parent, Citigroup) held $777 billion in deposits in domestic offices, of which $598.2 billion was uninsured. But wait for it Citibank also held a staggering $622.607 billion in deposits in foreign offices of which, potentially, nothing was insured according to current law and rulemaking. That would bring total deposits at Citibank in both domestic and foreign offices to $1.4 trillion with potentially only $178.8 billion FDIC insured or 13 percent. (We have sought clarification on this from the FDIC and will update this article when we receive a response.)

flight to safety, unintended consequences

https://wallstreetonparade.com/2023/...nterest-rates/On Sunday, Financial Times reporters Brooke Masters, Harriet Clarfelt and Kate Duguid published an article under the headline: “Money market funds swell by more than $286bn as investors pull deposits from banks.”

This article needs some important clarifications. First is the fact that money market funds had to be bailed out by the government during both the 2008 financial crisis and the more recent financial panic of 2020 stemming from the COVID pandemic.

On September 19, 2008 (four days after Lehman Brothers was placed into bankruptcy), stocks were crashing and investors were in a panic, the Department of the Treasury announced that it would provide a guarantee for money market mutual funds, standing behind more than $3.5 trillion in money market fund assets.

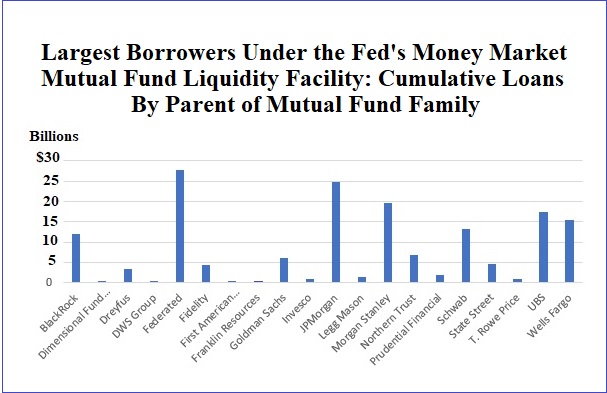

In mid-March 2020, as the share prices of mega banks on Wall Street were plunging in price and investors were in another panic, the Federal Reserve, with the required approval of the U.S. Treasury Secretary for emergency bailout programs from the Fed, established the Money Market Mutual Fund Liquidity Facility (MMLF). Under the facility, the Boston Fed made loans to various banks to purchase troubled assets from money market funds. When the Fed finally released the details of that program, Wall Street On Parade crunched the numbers and found that just six Wall Street firms received 72 percent of the $162.9 billion in ulative loans made under the MMLF. The three largest recipients were Federated, JPMorgan Chase and Morgan Stanley. (See our full report here.)

Most Americans are unaware that there are two vastly different kinds of money market vehicles. There is the “money market account” that one can hold at a federally-insured bank which is FDIC-insured up to $250,000 per depositor per bank. If you have multiple FDIC-insured accounts at the same bank (money market account, checking, savings, certificates of deposit), they all count toward the $250,000 insurance limit.

There is also the “money market fund” which is an uninsured mutual fund packed with short-term debt instruments of varying quality.

It was these uninsured money market funds that had to be bailed out during the 2008-2009 financial crisis on Wall Street and again during the March 2020 financial panic related to the COVID pandemic.

The Financial Times article is talking about the uninsured money market funds.

So why would Americans be flocking to these uninsured money market funds during the latest banking panic?

We found our answer in the data released by the Investment Company Ins ute (ICI.org). According to ICI’s statistics, $276.49 billion of that $286 billion reported by the Financial Times (or a whopping 97 percent), went into a very specific type of money market fund – the kind that holds short-term debt instruments guaranteed by the U.S. government. These are referred to as “government money market funds.”

ICI reports that total assets in Government Money Market Funds grew as follows in the month of March: total assets of $3.98 trillion as of March 9, 2023; total assets of $4.128 trillion as of March 15, 2023; total assets of $4.26 trillion on March 22, 2023.

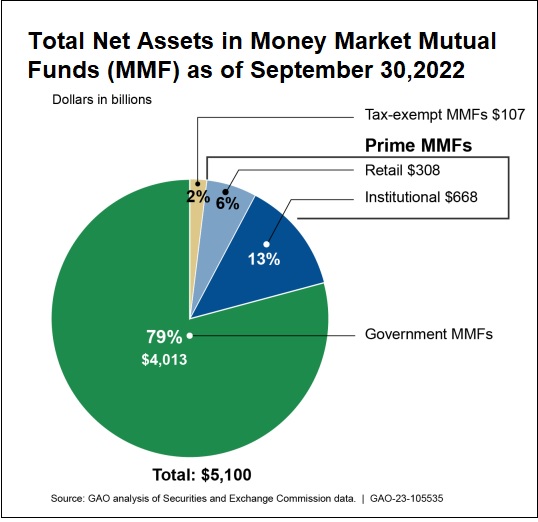

According to the ICI’s latest data, Government Money Market Funds in the U.S. now represent 83 percent of all money market funds. As of March 22, 2023, Government Money Market Fund assets of $4.26 trillion compared to total assets in all money market funds of $5.13 trillion. According to a report from the Government Accountability Office (GAO), Government Money Market Mutual Funds represented 79 percent of all money market funds as of September 30, 2022. (See chart below.)

This flight to safety is having an unintended consequence. It is throwing a wrench in the Federal Reserve’s plans to bring down inflation in the U.S. by hiking its benchmark interest rate. For example, the 6-month U.S. Treasury bill, which had traded at a yield of 5.29 percent in early March, is trading this morning at a yield of 4.85 percent – notwithstanding that the Fed raised its benchmark interest rate (Fed Funds) by another one-quarter percent on March 22.

Money market mutual funds are required to hold short-term instruments, typically of less than one year to maturity. Government Money Market Funds hold lots of U.S. Treasury bills, such as the 6-month T-bill. The demand for these government instruments of less than one year maturity, is also likely adding to the inverted yield curve, where short-term government securities are yielding significantly more than the 30-year U.S. government bond.

https://www.nakedcapitalism.com/2023...k-wobbles.htmlThere actually is an elegant solution to the problem of moral hazard, but bizarrely it has never gotten traction. The idea, first proposed by ex-Goldman partner William Dudley when head of the New York Fed, would have the effect of putting bank executives on a similar footing to old Wall Street partners by having most of their pay tied up for a number of years and acting as subordinate equity. If the bank’s equity was wiped out in a liquidation or a subsidized sale, they would take losses first, ahead of shareholders.

This general concept was refined by emeritus London School of Economics professor Charles Goodhart, who set forth a detailed conceptual scheme of how and how much “insiders” should have their compensation taken or clawed back in the event of a failure. Goodhart was more draconian than Dudley, suggesting that CEOs should face the loss of three times their total remuneration, and board members, two times. It’s a clever proposal, which you can read here.

FDIC isnt taxpayer funded

banks pay into it

surely you're not so naive as to think the banks don't pass along their costs of doing business to their customers?

excellent argument against raising taxes on corporations or the wealthy

they'll just pass it on

if that were the topic, but it isn't, and I'm not arguing that banks *not* bail in the FDIC.

looks like you've ceased on a distinction without much of a difference.

i agree, its a distinction without a difference, hence my point. you're making the exact same argument people make over corporate tax rates. the FDIC fund is a mandatory insurance buy-in akin to a tax on the banks. you argued that those costs are passed on to the customers anyway (in response to my contention that its not public funds and therefore not a public bailout). thats literally the same thing as the tax argument.

except, I'm not arguing against the bail in. that no money needs to be appropriated, yet, doesn't mean the receivership is cost free to the public. if the insurance fund gets tapped out, who will pay?

fintwit noise, I haven't been following this lately. Berkshire-Hathaway dumping all commercial bank stocks might not be a good sign,

https://x.com/porterstansb/status/1847379095367406050

There are currently 1 users browsing this thread. (0 members and 1 guests)

Posting Permissions

Posting Permissions