In November, 2002, two of the most significant flagships of the financial press, the German Handelsblatt and the American Wall Street Journal, had a brilliant idea: we will create, they said, a "shadow council", consisted of some of the most important academic economists, but also economists from the private sector. The council will conduct monthly meetings prior to the ECB board of directors, for the purpose to suggest whether the base interest rate should be increased, reduced, or, remain stable.

Despite the fact that this council has no ins utional characteristics, its existence as a consulting tool was planned by the Maastricht Treaty. Soon, it was transformed into an informal "ins ution", the decisions of which are reaching the headquarters of the ECB in Frankfurt.

Essentially, the target of this shadow council, as was mentioned sometime by Wall Street Journal, was to build a bridge for the big gap between the British central bank and the German Bundesbank.

From the first day, Handelsblatt's Norbert Häring, has been set the president and coordinator of the council. He participates in every meeting, without the right of voting. When I met him a few days ago in Brussels for the filming of the do entary

This is not a coup, I was prepared to face another passionate supporter of the European ins utions. Speaking at phone, however, he warned me that his view does not express the decisions of the shadow council. But there was nothing that could prepare me for the "bombs" he would attempt to plant at the euro-system foundations.

At the start of the interview, he told me that “

It is scandalous the fact that a central banker, like Stournaras, can state publicly that he had blocked the attempt of the [Greek] government to create a parallel currency, without ending in prison.” He also said that “

This time, we don't have a silent coup”, like in the case of Cyprus, Italy, or, Ireland, “

but a real coup that violates the responsibilities of the central bank and interferes [with] the political life of a country.”

According to Häring, the ECB has been transformed now into a powerful player who speaks directly with the biggest banks of the planet without being controlled [...] by the ins utional tools of the EU. He explains to me that “

The so-called independence of the ECB and of national banks is iconic. The fact that the elected governments are not able to affect ECB's decisions means that the influence of other players increases. I refer of course to the big financial ins utions. ECB always lies on the side of the big banks.”

According to Häring, ECB is able now to decide whether will sustain a government in power, or, will let this government collapse under the pressure of the markets - and that's exactly what happened with Berlusconi administration in Italy.

He says that “

The national central banks consist part of the ECB system and have a terrifying ability to blackmail governments.” Through the exchange of big bond packages, they provoke big interest rate fluctuations, forcing governments to give them anything they want in return. At the same time, “

they continuously give information to the ECB, through which it can blackmail the governments.”

Reply With Quote

Reply With Quote

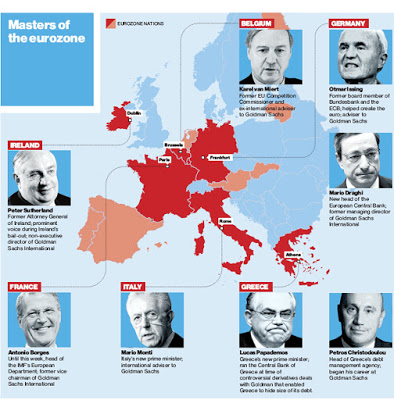

he Greek debt crisis offers another illustration of Wall Streets powers of persuasion and predation, although the Street is missing from most accounts.

he Greek debt crisis offers another illustration of Wall Streets powers of persuasion and predation, although the Street is missing from most accounts.