fixing Obamacare (but Repugs will object, obstruct, hold hearings, witch hunts!)

One of the necessary Obamacare fixes is about to be made, when the administration closes a loophole that has allowed large employer plans to still qualify under the law even if they don't offer hospitalization. With new regulations the Treasury Department is set to issue, that will end.\

The administration intends to disallow plans that "fail to provide substantial coverage for in-patient hospitalization services or for physician services," the Treasury Department said in a notice Tuesday morning. It will issue final regulations banning such insurance next year, it said.Hundreds of lower-wage employers such as retailers and temporary-staffing companies have been preparing to offer such plans for 2015, the first year large companies are liable for fines if they dont provide minimum coverage. Some have enrolled workers for insurance beginning Oct. 1.http://www.dailykos.com/story/2014/1...e?detail=email

For employers that have committed as of Nov. 4 to such coverage, the administration will temporarily allow it under the health law, the notice said.

One of the architects of ACA speaks candidly

"This bill was written in a tortured way to make sure the CBO did not score the mandate as taxes. If CBO scored the mandate as taxes, the bill dies."

"In terms of risk-rated subsidies, if you had a law which said that healthy people are going to pay in you made explicit healthy people pay in and sick people get money, it would not have passed."

"Lack of transparency is a huge political advantage. And basically, call it the stupidity of the American voter or whatever, but basically that was really really critical for the thing to pass."

Here Is What Will Happen If The Supreme Court Strikes Down Obamacares Subsidies

to understand the consequences of stripping away subsidies from the 5.4 million Americans who are currently enrolled in insurance through a federal exchange and are receiving subsidies one only need to look at the table below from the RAND Corporation. The research group ran the numbers for what would happen if the subsidies simply went away and here is what it came up with:

In short: higher health care costs, lower enrollment, and a higher number of uninsured Americans.

Enrollees who are eligible for the laws subsidies with incomes between 100 and 400 percent of the federal poverty level pay no more than a fixed percentage of their income for the second-lowest-cost silver plan available in their rating area, RAND explains. This structure cushions enrollees against premium increases due to other peoples enrollment decisions and guards against a cycle of premium increases and subsequent disenrollment.

Take that away and these five things will happen:

1. Millions of people will see triple digit premium hikes.

87 percent of the 5.4 million people enrolled in the federal marketplaces picked a plan using federal tax credits, lowering the amount of what they paid for their monthly premium from $346 to $82, on average. Without the tax credits, these families would be paying an average of $264 more per month, a 322 percent increase. Analysis from the Kaiser Family Foundation has also found that most of the individuals receiving subsidies are working families without access to employer-based coverage, earning between 200 and 300 percent of the federal poverty level. The subsidies paid for more than three-quarters of the cost of their premiums making it unlikely that they would be able to afford insurance otherwise.

2. Millions of people will lose health care coverage.

The Urban Ins ute estimate of eliminating subsidies from federally-run exchanges found that 7.3 million people could lose out on $36.1 billion in subsidies by 2016.

3. Obamacare will face a death spiral.

The RAND study found that in scenarios in which the tax credits are eliminated, our model predicts a near death spiral, with very sharp premium increases and drastic declines in individual market enrollment. Health economists believe that sick people who need care will sign up for coverage, no matter the cost. Healthy people generally dont and so the individual health care mandate and the subsidies act as inducements to encourage that group to enroll in coverage and balance out the cost of providing insurance to the sick. Eliminating the subsidies increases costs and discourages healthy people from remaining insured, leading to even higher premium increases and a very expensive risk pool full of sicker and by definition more expensive beneficiaries.

4. Insurers will advocate for repealing market protections.

Currently, insurers are prohibited from discriminating against individual with pre-existing health conditions and must offer everyone coverage at an average community rate. (Sick people or women cannot be charged more for coverage, for instance). But, if the pool of beneficiaries shrinks as coverage without subsidies becomes too expensive for healthy individuals, insurers will likely advocate to repeal these protections. The industry hasspent millions on lobbying and political contributions guaranteeing that Congress will be more than happy to listen to its demands.

5. States will lose billions of dollars.

Without subsidies, families and individuals would lose $36.1 billion worth of subsidies in 2016, the Urban Ins ute estimates. These dollars trickle down to health care providers and have a sizable impact on state economies. Losses would be as high as $4.8 billion in Florida and $5.6 billion in Texas, Urban estimates and would especially hurt the states refusing to expand their Medicaid programs. Those states are already foregoing large amounts of federal dollars while their providers are experiencing the Medicare and Medicaid payment cuts included in the law.

6. The health of Americans living in red states will worsen.

While states with state-run marketplaces wont experience a disruption, those that allowed the federal government to build their exchanges will. The latter are mostly run by Republican-leaning lawmakers and already have higher numbers of uninsured on average. A ruling in favor of the plaintiffs would thus perpetuate a health care divide between so-called blue and red states.

http://thinkprogress.org/health/2014/11/08/3590572/the-6-biggest-consequences-of-the-supreme-court-striking-down-obamacares-subsidies/

why would be bill die (no Repugs voted for it) if mandate was considered a tax?

"if you had a law which said that healthy people are going to pay in " that's not what ACA is, so shut up. older (sicker) people pay more than younger (less sick, but still sick) people, everybody's covered.

HE can call it the stupidity of the American voter, but ACA was not passed in a citizen's general referendum, it was passed DEMOCRATS' Congresscritters, so the stupidity of the American people is a stupid comment.

And since when does an extreme right-winger whine or worry about "stupidity of the American people" when the entirety of right-wing politics is based on that stupidity, ignorance, ideological/religious fantasies of its voters?

Last edited by boutons_deux; 11-10-2014 at 11:55 AM.

I honestly dont remember why I said that. I was speaking off-the-cuff. It was just a mistake. People make mistakes. Congress made a mistake drafting the law and I made a mistake talking about it.

During this era, at this time, the federal government was trying to encourage as many states as possible to set up their exchanges. ...

At this time, there was also substantial uncertainty about whether the federal backstop would be ready on time for 2014. I might have been thinking that if the federal backstop wasn't ready by 2014, and states hadn't set up their own exchange, there was a risk that citizens couldn't get the tax credits right away. ...

But there was never any intention to literally withhold money, to withhold tax credits, from the states that didnt take that step. Thats clear in the intent of the law and if you talk to anybody who worked on the law. My subsequent statement was just a speak-oyou know, like a typo.

There are few people who worked as closely with Obama administration and Congress as I did, and at no point was it ever even implied that thered be differential tax credits based on whether the states set up their own exchange. And that was the basis of all the modeling I did, and that was the basis of any sensible analysis of this law thats been done by any expert, left and right.

I didnt assume every state would set up its own exchanges but I assumed that subsidies would be available in every state. It was never contemplated by anybody who modeled or worked on this law that availability of subsides would be conditional of who ran the exchanges.

http://www.newrepublic.com/article/1...es-was-mistake

Study: Pre-Obamacare Health Insurance Was Better Quality Than Exchange Plans

http://dailycaller.com/2014/09/15/st...xchange-plans/

Individual health insurance policies were of higher quality in 2013, before Obamacare regulations hit, than the offerings on health-care exchanges this year, according to a study released Monday.

The National Center for Public Policy Research examined the health insurance plans available before the health care law took effect in ten major cities and found that for 27 year-olds and 57 year-old couples, the individual market used to provide more comprehensive coverage than the exchanges.

As is typically the case with Obamacare, young adults were the hardest hit. Last year, there was an average of 33 health insurance plans in each area studied that offered not only lower premiums than the least expensive Obamacare plans currently available, but also lower or equal deductibles and out-of-pocket costs.

Older adults have a similar experience. There’s an average of 10 policies per area that had lower premiums and deductibles last year, compared to the cheapest exchange offerings this year.

Cost isn’t the only factor, either. The study found that Obamacare exchanges are populated by more restrictive types of health insurance — significantly more so than the individual market was in 2013. (RELATED: Insurer: Obamacare Customers Must Break ‘Choice Habit’)

Health maintenance organizations (HMOs) are generally the most restrictive type of provider network, where the insurance company doesn’t cover out-of-network providers at all, according to the study. Preferred provider organizations (PPOs), usually cover out-of-network providers, but require patients to pay higher cost-sharing for it, giving patients the widest range of options to choose their doctors.

While Obamacare exchanges have already become infamous for offering significantly narrower networks than are common in the individual and employer-based health insurance markets, the exchanges in these areas also have a higher proportion of more restrictive HMO plans, which don’t pay for any care outside the already-shrunken network. Obamacare exchanges had an average of 16 more HMO plans for both age groups.

The 2013 private individual market boasted 32 more less-restrictive PPO plans for 27 year-olds compared to Obamacare exchanges, and 25 more plans on average for 57 year-olds. (RELATED: Obamacare-Forced Narrow Networks Will Spread To The Whole Country, Expert Warns)

“When millions of people were losing their health insurance plans in late 2013, Obamacare supporters claimed those plans were of poor quality, calling them substandard and even ‘crappy,’” Dr. David Hogberg, the study’s author, said in a statement. “But they never provided any evidence to support those claims. Quite the contrary, this study shows that in important ways, the plans on the individual market in 2013 were of better quality than those on the Obamacare exchanges.”

While Obamacare supporters have long charged that the health insurance industry was filled with “junk” insurance plans instead of quality plans, the market appears to have had quite a few advantages over the Affordable Care Act’s first year of offerings.

Either way, customers may be more satisfied with the lower-cost coverage they had before the health-care law. One Kaiser Family Foundation survey found customers were happier with plans that weren’t compliant with Obamacare regulations than they are with Obamacare-approved insurance plans.

just another anti-government, anti-Dem, bogus VRWC stink tank

"TheNational Center for Public Policy Research, founded in 1982, is a self-described conservative think tank in the United States."

http://en.wikipedia.org/wiki/Nationa...olicy_Research

"young adults hardest hit" while being covered on their parents' plans until age 26?

etc, etc, etc. Pure VRWC bull , as expected from TLong.

The truth hurts doesn't it boo?

truth! you posted .

what about 20M Americans who now have Medicaid coverage?

children covered by parents to age 26?

by more transparency of health costs?

the illegal junk insurance plans?

the blocking of insureres denying to insure sick people?

etc, etc, etc.

your " " above is propaganda from a VRWC stink tank, not the truth.

, meet slap!

The Affordable Care Act & Medicare

Top 5 things to know about the Affordable Care Act (ACA) if you have Medicare:

- Your Medicare coverage is protected.Medicare isnt part of the Health Insurance Marketplace established by ACA, so you don't have to replace your Medicare coverage with Marketplace coverage. No matter how you get Medicare, whether through Original Medicare or a Medicare Advantage Plan, youll still have the same benefits and security you have now.

You dont need to do anything with the Marketplace during Open Enrollment.

- You get more preventive services, for less. Medicare now covers certain preventive services, like mammograms or colonoscopies, without charging you for the Part B coinsurance or deductible. You also can get a free yearly "Wellness" visit.

- You can save money on brand-name drugs. If youre in the donut hole, you'll also get a 55% discount when buying Part D-covered brand-name prescription drugs. The discount is applied automatically at the counter of your pharmacyyou dont have to do anything to get it. The donut hole will be closed completely by 2020.

- Your doctor gets more support. With new initiatives to support care coordination, your doctor may get additional resources to make sure that your treatments are consistent.

- The ACA ensures the protection of Medicare for years to come.The life of the Medicare Trust fund will be extended to at least 2029a 12-year extension due to reductions in waste, fraud and abuse, and Medicare costs, which will provide you with future savings on your premiums and coinsurance.

http://www.medicare.gov/about-us/aff...-care-act.html

Health Premiums Up $3,065; Obama Vowed $2,500 Cut

http://finance.yahoo.com/news/health...224300715.html

During his first run for president, Barack Obama made one very specific promise to voters: He would cut health insurance premiums for families by $2,500, and do so in his first term.

But it turns out that family premiums have increased by more than $3,000 since Obama's vow, according to the latest annual Kaiser Family Foundation employee health benefits survey.

Premiums for employer-provided family coverage rose $3,065 24% from 2008 to 2012, the Kaiser survey found. Even if you start counting in 2009, premiums have climbed $2,370.

What's more, premiums climbed faster in Obama's four years than they did in the previous four under President Bush, the survey data show.

There's no question about what Obama was promising the country, since he repeated it constantly during his 2008 campaign.

In a debate with Sen. John McCain, for example, Obama said "the only thing we're going to try to do is lower costs so that those cost savings are passed onto you. And we estimate we can cut the average family's premium by about $2,500 per year.

At a campaign stop in Columbus, Ohio, in February 2008, Obama promised that "We are going to work with you to lower your premiums by $2,500. We will not wait 20 years from now to do it, or 10 years from now to do it. We will do it by the end of my first term as president.

2008 Promises, 2012 Reality

To back that up, Obama pointed to a memo drafted by Harvard professors (and unpaid campaign advisers), which claimed that investing in health care IT, cutting administrative bloat, and improving management of chronic diseases would cut health costs by $140 billion a year. That would translate into $2,500 in premium savings for families.

But those projections were wildly optimistic, overestimating potential savings from IT, making big assumptions about disease management, and ignoring the fact that past government interventions have always increased health care administrative costs.

Meanwhile, the health reform law Obama signed in March 2010 has pushed up insurance costs.

In 2011, premiums ed 9.5%, and many in the industry blame ObamaCare for at least part of it. Premiums climbed another 4.5% in 2012, Kaiser found.

And ObamaCare will continue to fuel health premium inflation.

First, the law piles on new coverage mandates. It requires insurance companies to provide 100% coverage for various types of preventive care, bans lifetime coverage limits, extends parents' coverage to offspring up to 26 years old, and requires plans to meet certain "medical loss ratios." Coming up are rules on "essential standard benefits," limits on deductibles, bans on annual spending caps, and much more.

The experience with state mandates show that they only tend to grow over time, and get more expensive. The Council for Affordable Health Insurance found more than 2,200 state benefit mandates, which add from 10% to 50% to the cost of coverage.

"One of the biggest cost drivers in our health care system is the steady proliferation of federal and state-based coverage mandates," noted CAHI's Victoria Craig Bunce.

Meanwhile, ObamaCare's insurance reforms guaranteed issue and community rating will likely raise premiums, too.

State Experiments

States that have tried these reforms which forbid insurers from denying coverage based on preexisting conditions or charging the sick more have seen insurance premiums spiral upward as healthy people leave the market, knowing they are guaranteed coverage when they get sick.

"Premium rates tended to increase, sometimes dramatically" in the eight states that tried these reforms, according to a study by Milliman, a health care consulting group.

The law's backers claim the individual mandate will prevent these rate hikes, because it requires everyone to buy insur ance. But experts say millions will still refuse to buy coverage and pay the fine instead.

Meanwhile, Jonathan Gruber who helped design ObamaCare found that the law will hike individual market premiums in three states by as much as 30%. The Congressional Budget Office said ObamaCare would push them "about 10% to 13% higher in 2016." Supporters say people will be getting more generous coverage for those higher prices, and that tax subsidies will offset higher cost for many of these families. But that will be small comfort to those forced to pay more.

Perhaps the best evidence that ObamaCare won't bring costs down is a report published this month in the New England Journal of Medicine and signed by nearly two dozen leading health economists and policy experts some of whom worked for the Obama administration. The report warns that "health costs remain a major challenge" and calls for a "systematic approach" to get spending under control.

One thing that isn't on their list of proposals: Scrapping Obama-Care and starting over.

Last edited by tlongII; 11-10-2014 at 06:13 PM.

"The report warns that "health costs remain a major challenge" and calls for a "systematic approach" to get spending under control."

ACA doesn't set health care cost, price of insurance policies.

the health care industry has been raping America for decades. That's not ACA's fault

SCOTUS takes up a Halbig challenge, to rule by July 1:

http://healthpolicyandmarket.blogspo...e-subsidy.htmlIn a Wow moment, the Supreme Court announced Friday that they will take one of the four pending "Halbig" cases––specifically King v. Burwell.

The issue is over whether the new health law actually authorizes the payment of premium subsidies in the 37 states that will rely upon the federal government to run their exchange in 2015.

This effort is being made on a number of fronts but has been generally know as the "Halbig" challenge. I guess we will now call it the King challenge.

If the Supreme Court eventually affirms this challenge, anyone receiving a health insurance subsidy in the 37 states run by the feds would immediately lose it. Given that the bulk of those currently getting subsides are at the lower income range for those subsidy eligible, most would likely drop their Obamacare insurance unless they were so sick it made sense for them to beg, borrow, or steal the money they would need to continue making premium payments.

The result would be a much smaller Obamacare insurance pool disproportionately filled with sick people.

http://www.nytimes.com/2014/11/08/up...care-case.htmlStill, it’s worth remembering all of the parts of the health law that are not under attack by this case. The Medicaid expansions, now underway in 27 states, would stand. Young adults would still be able to get coverage through their parents’ health insurance. The law’s reforms of Medicare payment policy would stay on the books. Regulations on insurance companies limiting their profits and requiring that all products cover certain basic benefits would stay in effect. And the subsidies flowing to states that ran their own exchanges would continue.

An anti-Obamacare decision in the King case wouldn’t take the health law off the books. It would just make federal spending on health care more uneven than it already is.

Death by Typo

My parents used to own a small house with a large backyard, in which my mother cultivated a beautiful garden. At some point, however I dont remember why my father looked at the official deed defining their property, and received a shock. According to the text, the Krugman lot wasnt a rough rectangle; it was a triangle more than a hundred feet long but only around a yard wide at the base.

On examination, it was clear what had happened: Whoever wrote down the lots description had somehow skipped a clause. And of course the town clerk fixed the language. After all, it would have been ludicrous and cruel to take away most of my parents property on the basis of sloppy drafting, when the drafters intention was perfectly clear.

But it now appears possible that the Supreme Court may be willing to deprive millions of Americans of health care on the basis of an equally obvious typo. And if you think this possibility has anything to do with serious legal reasoning, as opposed to rabid partisanship, I have a long, skinny, unbuildable piece of land you might want to buy.

Last week the court shocked many observers by saying that it was willing to hear a case claiming that the wording of one clause in the Affordable Care Act sets drastic limits on subsidies to Americans who buy health insurance. Its a ridiculous claim; not only is it clear from everything else in the act that there was no intention to set such limits, you can ask the people who drafted the law what they intended, and it wasnt what the plaintiffs claim. But the fact that the suit is ridiculous is no guarantee that it wont succeed not in an environment in which all too many Republican judges have made it clear that partisan loyalty trumps respect for the rule of law.

To understand the issue, you need to understand the structure of health reform. The Affordable Care Act tries to establish more-or-less universal coverage through a three-legged stool of policies, all of which are needed to make the system work. First, insurance companies are no longer allowed to discriminate against Americans based on their medical history, so that they cant deny coverage or impose exorbitant premiums on people with pre-existing conditions. Second, everyone is required to buy insurance, to ensure that the healthy dont wait until they get sick to join up. Finally, there are subsidies to lower-income Americans to make the insurance theyre required to buy affordable.

Just as an aside, so far this system seems to be working very well. Enrollment is running above expectations, premiums well below, and more insurance companies are flocking to the market.

So whats the problem? To receive subsidies, Americans must buy insurance through so-called exchanges, government-run marketplaces. These exchanges, in turn, take two forms. Many states have chosen to run their own exchanges, like Covered California or Kentuckys Kynect. Other states, however mainly those under G.O.P. control have refused to take an active role in insuring the uninsured, and defaulted to exchanges run by the federal government (which are working well now that the original software problems have been resolved).

But if you look at the specific language authorizing those subsidies, it could be taken by an incredibly hostile reader to say that theyre available only to Americans using state-run exchanges, not to those using the federal exchanges.

As I said, everything else in the act makes it clear that this was not the drafters intention, and in any case you can ask them directly, and theyll tell you that this was nothing but sloppy language.

Furthermore, the consequences if the suit were to prevail would be grotesque. States like California that run their own exchanges would be unaffected. But in places like New Jersey, where G.O.P. politicians refused to take a role, premiums would soar, healthy individuals would drop out, and health reform would go into a death spiral. (And since many people would lose crucial, lifesaving coverage, the deaths wouldnt be just a metaphor.)

Now, states could avoid this death spiral by establishing exchanges which might involve nothing more than setting up links to the federal exchange. But how did we get to this point?

Once upon a time, this lawsuit would have been literally laughed out of court. Instead, however, it has actually been upheld in some lower courts, on straight party-line votes and

the willingness of the Supremes to hear it is a bad omen.

So lets be clear about whats happening here.

Judges who support this cruel absurdity arent stupid; they know what theyre doing.

What they are, instead, is corrupt, willing to pervert the law to serve political masters.

And what well find out in the months ahead is how deep the corruption goes.

http://www.nytimes.com/2014/11/10/op...obamacare.html

Not a Typo, but I totally support the government's position here.

http://ziffblog.wordpress.com/2014/1...ca-litigation/

Obviously Kruggy using typo as a MISstatement 100% incompatible with the totality of the ACA law.

This is nothing but Repug/conservative BAD FAITH, smash-mouth, scorched earth destructive politicking.

I read one article that suggested Roberts could now repeat what he did in saving ACA: save the ACA, but at the same time reduce federal power in the states (eg, allow the states to say no to Medicaid expansion and over their poor citizens (esp blacks and browns, but of course Ms of whites, too), making Repugs and conservatives everywhere happy to over Human-Americans). Repugs are nothing if not "states rights" racists.

Last edited by boutons_deux; 11-14-2014 at 04:52 PM.

suck it, punks

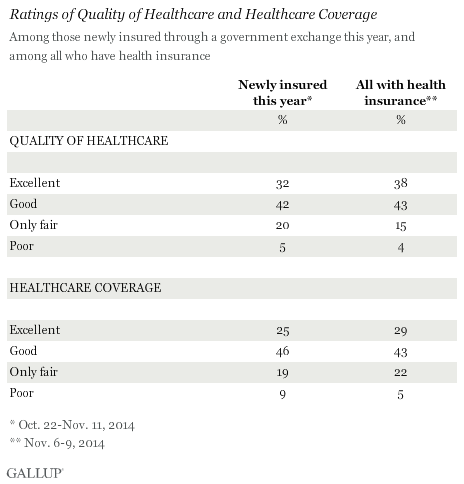

Newly Insured Through Exchanges Give Coverage Good Marks

http://www.gallup.com/poll/179396/ne...ood-marks.aspx

so you say "suck it" and then provide a chart that shows the new healthcare recipients aren't better off than the general insured population, and more likely to be worse off. cool.

suck it,

ACA works for people it was intended to help, in spite of your Repugs killing 1000s of their redstate victims by denying them health care.

And the "general population" is "better off"/screwed by the predatory, greedy, gouging health care system. "free market" delivering the tiest possible product for highest possible price.

btw, BigPharma, already pouring $Bs of drugs into school kids, is now pushing hard to add the anti-psychotic Abilify, outselling all other prescription drugs at $7B/year, to kids already taking ADHD drugs.

Of course, Abilify hasn't been tested on kids, and nobody knows really how Abilify works.

not here in Texas it doesn't:ACA works for people it was intended to help, in spite of your Repugs killing 1000s of their redstate victims by denying them health care.

http://my.firedoglake.com/blog/2014/...-aca-in-texas/Since our yearly income is too low for a tax credit, I was anxious to locate an affordable plan, for purchase. I reasoned that there might be coverage available that would be affordable, in case of a catastrophic event, in the least. My husband and I could figure the cost for purchasing the plan into a new monthly budget that we are working on, given our recent move to Texas. After completing my application, the healthcare.gov site directed me to an available 33 plans for purchase. Not one plan is affordable. In fact, some of the plans exceed or nearly exceed our monthly income. The lowest-cost plan available calls for nearly half of our monthly income, just for the premium. The deductible is roughly equivalent to one-half of our yearly income. Were I to schedule, for example, a monthly visit to a regular doctor, I would still have to pay cash for every single visit, without even coming close to meeting the deductible. Here is an example, taken directly from the list of choices in my application this morning:

CatastrophicIf I get sick, and I have the catastrophic plan, which I cannot afford to have, I will have to pay $612.62 plus $40 plus $6000, in order to receive one single generic antibiotic tablet, let alone receive any care for a real catastrophe. At the other end of the spectrum, the best plan available, there is this:

Covers less than 60% of the total average costs of care: $612.62/month

Deductible $6,600 Outofpocket maximum $6,600

Copayments / Coinsurance $40 Primary doctor

No Charge After Deductible Specialist doctor

No Charge After Deductible Generic prescription

Health care costsThis yearly premium is only slightly less than our yearly income, and it does not provide full coverage. In addition, the list of medications that are covered in this best-case scenario, is limited. When I called the 800-number and spoke to a representative this morning, I asked what I should do, to prepare for the possibility of a catastrophic event, such as an accident or severe illness. She told me that I could go to a local clinic and apply for a card, so that in the event of an accident, I can present the card, and maybe qualify to be taken to a local health clinic (not a hospital), but even this is not guaranteed.

Plan covers 80% of total average cost of care

Yearly premium

$12,559.56

When we first moved here, I stopped by an office to inquire about low-income options for health insurance such as Medicaid, but I do not qualify. Entry-level jobs that I have applied for do not offer benefits, and the wages are too low to be able to purchase even the least expensive, catastrophic plan.

I am ineligible to qualify for Medicaid, but too poor to purchase health insurance, because Texas refused the billions of dollars it was offered, in federal subsidies. Not only that, but if it werent for filling out an application this morning and receiving an exemption code, I would be fined, for not signing up for unaffordable government health insurance, that provides no benefits.

Insurers screwing Human-Americans isn't ACA's fault. ACA needs a lot of fixing, but Repugs, esp TX Repugs, prefer to screw their citizens (to death) by not expanding Medicaid, by not allowing ANY fixes to ACA.

There are currently 1 users browsing this thread. (0 members and 1 guests)

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote