Reply With Quote

Reply With Quote

Why?

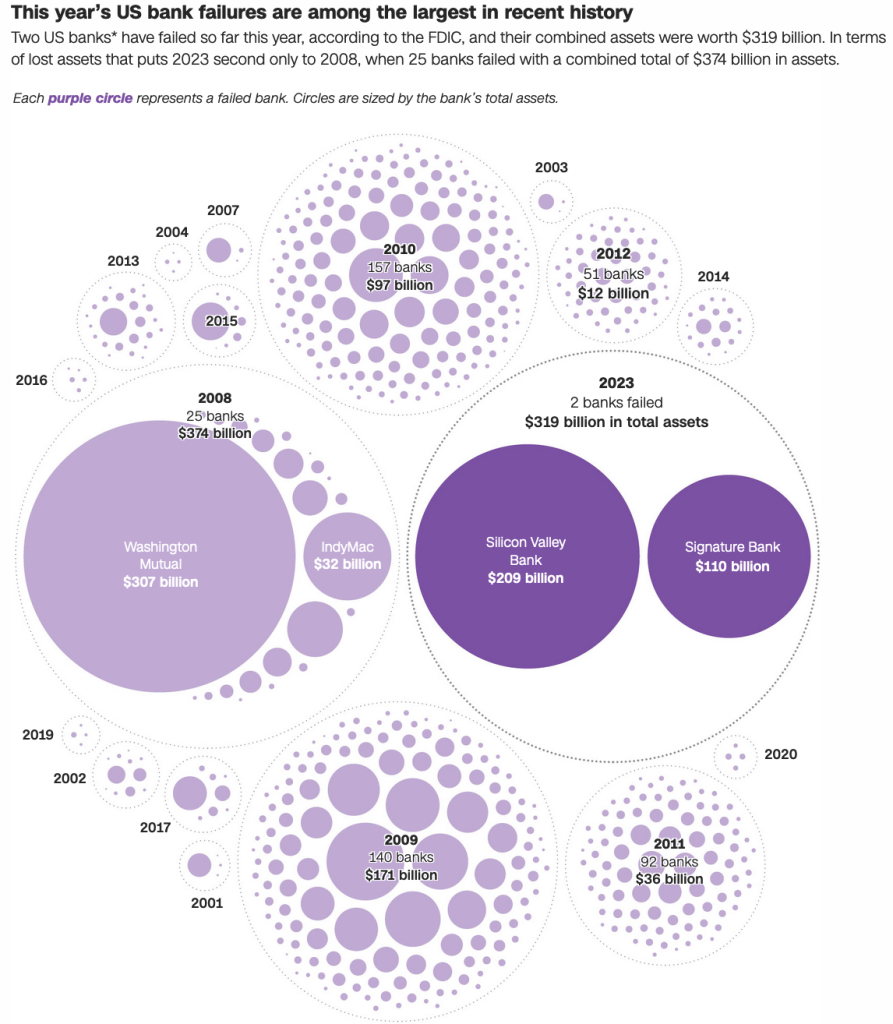

To make insolvent banks whole in 2008-9 rather than saving millions of homeowners, to save business and the system of payment in the global COVID demand shock in 2020-1, and who knows why in 2019.

It happened twice within this generation: In 2008-9 and 2020-1, as the whole world recalls. Less mentioned is 2019.And just lol at the idea that Dodd Frank was a paradigm shift that dominated the banks (never mind newly dubbed nonbanks, i.e., the shadow banking system, hedge funds, esrwhile broker-dealers and so forth) and solved the problems exposed in 2008. Not only was it business as usual, it was business as usual on steroids, with the Fed shoving trillions at the banks and nonbanks through the various forms of QE and exotic bespoke lending facilities. And arbitrage opportunities presented by 15 years of zero bound interest rates.

And while it's true none of that money had to be appropriated by Congress and represents a nominal zero cost to taxpayers, the inflation of various asset classes and economic sectors was real, and imposed real costs, for example in housing. Not having to write down bad debt to market value in 2008 kept prices high, financial speculation subsequently put it out of reach for the middle class.

https://www.spurstalk.com/forums/sho...1#post10875226

Why?

To make insolvent banks whole in 2008-9 rather than saving millions of homeowners, to save business and the system of payment in the global COVID demand shock in 2020-1, and who knows why in 2019.

Last edited by Winehole23; 03-19-2023 at 02:44 AM.

One way to read this is capitalism broke three times in 15 years. Once was due to epochal fraud and greed, twice was an epochal pandemic.

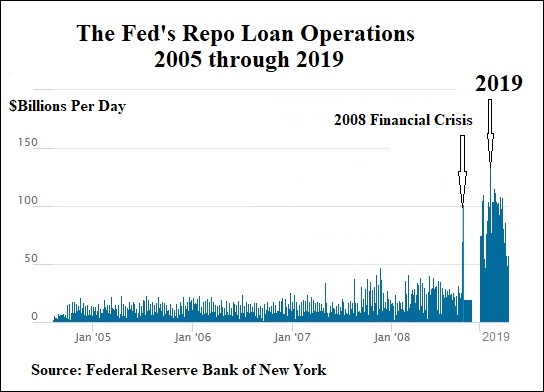

Who knows what the 2019- trend means.

yup

Damn, qchrisy woke up extra thirsty and gullible today.

Dodd frank didnt solve everything but was a step in the right direction. And complaining about housing inflation post 2008 is odd considering what it looked like pre 2008

Another problem "solved":

Galaxy brain wants a safe space.

Oh. There was a big housing bubble before. It was all over the news

not sure how that speaks to affordability now, still don't see your point.

"Standard procedure"

If we consider 2008 and 2020 standard.

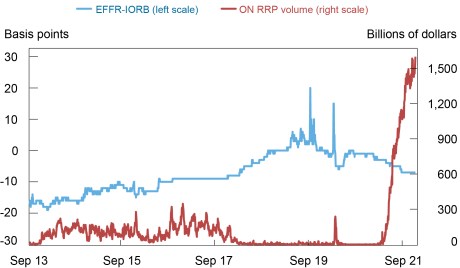

Is it standard for the system of payment to get stressed like this now?

Or for the US to lean on foreign central banks to maintain USD deposits?

Before Collapse of Silicon Valley Bank, the Fed Spotted Big Problems

https://www.nytimes.com/2023/03/19/b...lley-bank.html

pretty much. Fed may not have to tap the brakes much if this damps VC enough.

translation:

biden biden something something Hunter's , something China something

you really will believe anything.

Amused to see the "not a bailout" usage elsewhere

Fingers crossed, grandiose efforts to make people feel more secure can backfire. The bigger the effort, the bigger the implied problem is. If the market subsequently takes a on confidence building measures, insecurity and mistrust are amplified.

https://www.usatoday.com/story/money...l/11504269002/On the heels of Silicon Valley Banks collapse earlier this month, 186 more banks are at risk of failure even if only half of their depositors decide to withdraw their funds, a new study has found.

That is because the Federal Reserves aggressive interest rate hikes to tamp down inflation have eroded the value of bank assets such as government bonds and mortgage-backed securities.

The recent declines in bank asset values very significantly increased the fragility of the U.S. banking system to uninsured depositor runs, economists wrote in a recent paper published on the Social Science Research Network.

Shady accounting, exposure to derivatives

https://www.nakedcapitalism.com/2023...ers-worse.htmlKeeping in mind that both of Switzerland’s behemoths, UBS and Credit Suisse, got in a heap of trouble in the crisis, with UBS being one of the most enthusiastically self-destructive users of CDOs. Not only did they eat a lot of their own bad cooking, but they were a leader in the so-called negative basis trade, which was a spectacular form of looting. The short version is traders bought other people’s CDOs, supposedly insured them with credit default swaps, and then got to book all the expected future profit in the current P&L and get paid bonuses on those fictive profits.

Finally, back to a main point, that yet more subsidies of banks will simply enable more incompetence and looting absent getting bloody-minded regulators, a prospect that seems vanishingly unlikely.

Elizabeth Warren is again taking up her bully pulpit of calling for more bank reform, but technocratic fixes are inadequate with a culture of timid enforcement. The only remedy in all the years I have read about that might have a real impact quickly creates real skin in the game. It proposed by of all people former Goldmanite, later head of the New York Fed William Dudley.

Dudley recommended putting most of executive and board bonuses in a deferred account, IIRC on a rolling five-year basis. If a bank failed, was merged as part of a regulatory intervention, or wound up getting government support, the deferred bonus pool would be liquidated first, even before shareholder equity. Skin in the game would do a lot more to curb reckless behavior than complex new rules.

There are currently 1 users browsing this thread. (0 members and 1 guests)

Posting Permissions

Posting Permissions