Mortgage underwriting: There were obvious crimes committed in mortgage underwriting, where defects were

knowingly ignored. The

FBI investigated these cases early on, but investigators never moved forward with prosecutions.

Perhaps the scale of the financial penalties bank agreed to pay had something to do with this inaction. Keefe, Bruyette and Woods, tallied the

financial-crisis related regulatory penalties the total was a

staggering $243 billion.

Accounting fraud: We could spend months discussing how some executives at banks

cooked their books, but look no further then Lehman Brothers infamous Repo 105. That was a textbook example of defrauding the investing public by hiding the conditions of your insolvency.

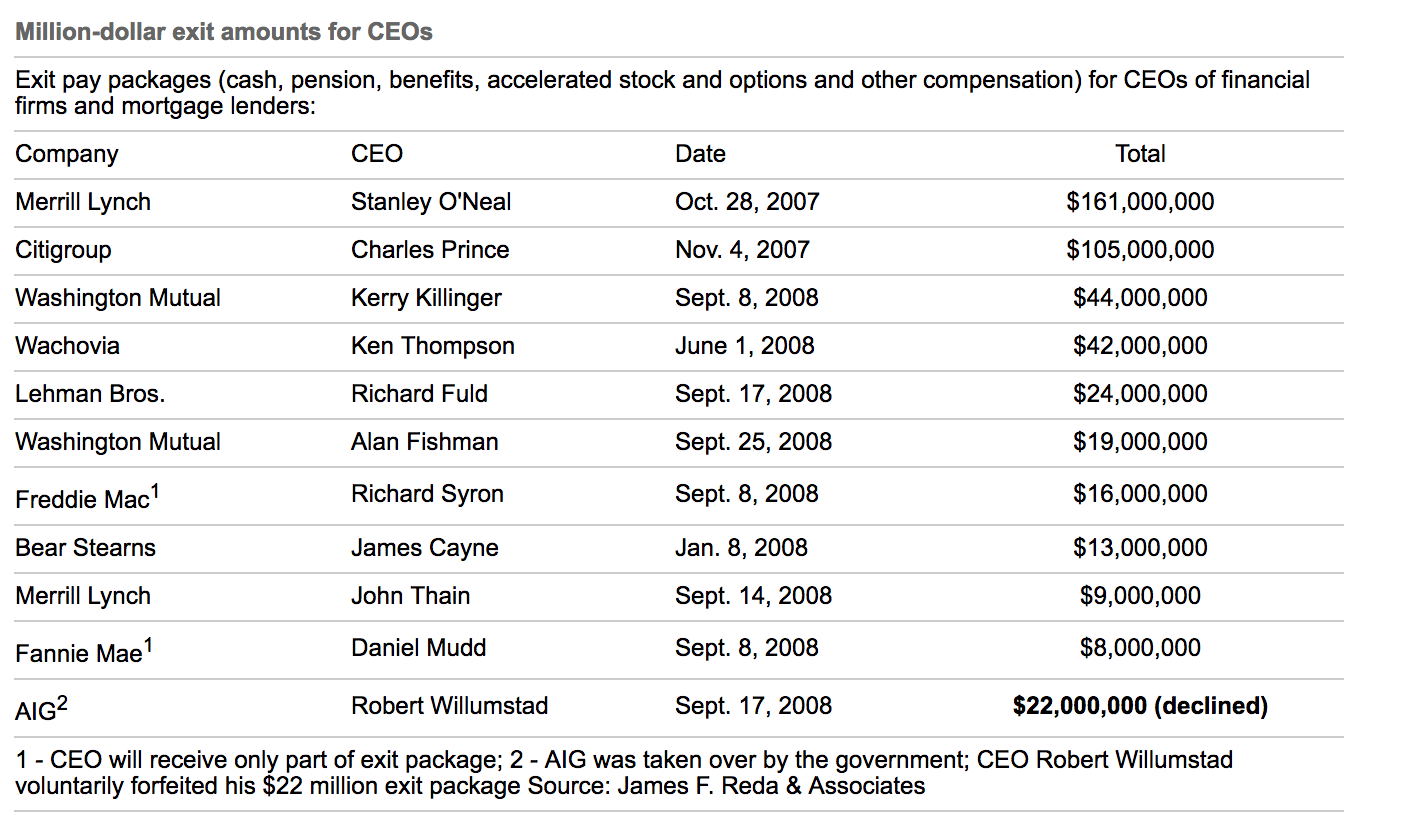

Insider Trading: Take a close look at insider stock sales during the period right before the crisis.

Sure seems like a lot of selling an a hurry . . . I wonder why?

David DeBoskey, a San Diego State University professor of Accountancy (and a KPMG Faculty Fellow), found

total compensation for top executives at just 4 of the firms that collapsed Lehman, AIG, Fannie Mae and Freddie Mac was

in excess of $1.4 billion dollars from 2003 to 2007.8 That much stock being sold before share prices collapsed was apparently a mere coincidence.9

Foreclosure fraud: There was a huge paper train showing fabricated do ents, falsified paperwork, and other perjury. Of all the crimes committed duri

ng the financial crisis and in its aftermath, this is one that should have been the easiest to identify and prosecute.

Reply With Quote

Reply With Quote