lol house flipping shoes

tbh I set very little store by official announcements be they corporate or political. none of them are accurate: at best, they represent enlightened guesses.

imminent domain rears it's ugly head in California: http://gawker.com/a-housing-crisis-s...reet-963479870

this is a wonderful move. I'm pretty sure Mortgage Resolution Partners has done its legal homework.

Financial sector stole 4M homes (and fraudulent MERS still exists), it's way past time for the people to the lenders back.

imminent domain is supported by right wingers and corps to screw up people's property for pipelines or resource extraction, but if people use imminent domain, they get trashed.

the efficient market hypothesis is infallible

assuming the world is fair, politics stable, and all of the people in it motivated by rational self interest, absolutely infallible.

has ing all to with "markets", it's all about lawyering.

" all," as we say in English

are you suggesting the market's eye for the odds is dangerously myopic ?

economics isn't called the dismal science for nothing; all the explanations have been refuted by experience or soon will be.

perhaps our government and economists suffer from anosognosia.

that's not distinctive, so, probably, yes.

Beware Private Equity Guys Bearing Gifts: Eminent Domain Mortgage Scam Hit with Well-Deserved Lawsuit

But as weve written, the private equity firm Mortgage Resolution Partners looks to be well on its way to getting the good uses of eminent domain torpedoed by getting some not-too-swift municipalities to sign up for its self-serving scheme. One indicator of how dubious the MPR program is that investors who have been complacent in the face of all sorts of abuses by originators and servicers, have roused themselves to act in a unified manner and push back against the MRP plan, in the form of a suit filed in Federal court in California on Wednesday.

Key to understanding why this plan is a terrible idea and why investors are outraged is that there is a large gap between MRPs well-funded messaging and how its program would actually work. The key thing to understand is that MPRs plan isnt about helping distressed borrowers. If communities wanted to condemn delinquent or defaulted mortgages, they dont need MRP. It wouldnt be hard to find dozens of hedge funds and other investors to bid on them and their aim would be to restructure the loans.

And investors would be delighted to see this happen. Investors and homeowners lose in foreclosures. Both would do better with a modification, provided the borrower still has a reasonable income. Its the servicers who win by continuing to wring servicing, foreclosure-related, and junk fees out of the securitizations.

MRPs initial effort was with several government en ies in the San Bernardino, California area. They signed up with a plan to condemn performing mortgages, meaning ones where borrowers were paying on time. MRP and the San Bernardino cohort tried passing off the canard that because the homes were underwater, the mortgage was worth less than the value of the house. No, sports fans, with a collateralized loan, the collateral is a backup source of value. It reduces losses in the event of default. You look to the borrower payment stream as the primary source of value. These were all seasoned mortgages, five years or more of current payments. These are borrowers who are clearly committed to keeping their homes and have income to do so. An arms length transaction would allow for some risk of default due to death, disability, or job loss, so a mortgage with a face amount of $300,000 would not go for $300,000. But if you have a current borrower with a solid payment history, you wouldnt expect it to fetch much less than $250,000.

But the MRP scheme relied on condemning those mortgages at a large discount to their value by the bait and switch of claiming the mortgage value was based strictly on the value of the home, which is inaccurate, and then arguing for a discount from that. Look at how much the investors get ripped off, per this summary from Nick Iimiraos of the Wall Street Journal last year:

For a home with an existing $300,000 mortgage that now has a market value of $150,000, Mortgage Resolution Partners might argue the loan is worth only $120,000. If a judge agreed, the programs private financiers would fund the citys seizure of the loan, paying the current loan investors that reduced amount. Then, they could offer to help the homeowner refinance into a new $145,000 30-year mortgage backed by the Federal Housing Administration, which has a program allowing borrowers to have as little as 2.25% in equity. That would leave $25,000 in profit, minus the origination costs, to be divided between the city, Mortgage Resolution Partners and its investors.

The difference between my working figure of $250,000 and $120,000 is a whole chunk of change. You can see why investors are irate.

http://www.nakedcapitalism.com/2013/...+capitalism%29

Congress forced changes in underwriting for loans?

Your calls for intelligent debating on the internets would ahve more gravitas, were you to stop running away from the indefensibily stupid threads you start.

Last edited by RandomGuy; 08-08-2013 at 02:19 PM. Reason: killingn typos

1. I wouldn't run. I would yell fire and sneak away.

2. All my threads are classics in their own right. As if walt whitman were blogging.

ftr you did it again. as if on cue

Forced? no. Allowed? yes.

It was mentioned by snakeboy upstream that congress had been asked to examine this....to no avail.

as the charts above show, unregulated private lenders, aka shadow bankers, wrote a lot of ty mortgages, probably with lots of capital freed up with dubya's tax cuts on the wealthy.

Congress was not involved "allowing". dubya actually shutdown the attempt by 19 states' AGs to stop predatory lending (and then Wall St got dubya to take down Spitzer)

Again.

http://www.spurstalk.com/forums/show...=1#post5483842

Subsequent posts by WH shows that congress was very much involved.

Fed to reduce MBS holdings to zero?

https://wolfstreet.com/2018/05/16/wi...o-be-the-plan/

non-bank mortgage lending at pre-crisis levels in 2018:

https://www.brookings.edu/wp-content.../5_kimetal.pdfMuch less understood, and largely absent from the standard narratives, is the role playedby liquidity crises in the nonbank mortgage sector. While important post-crisis research did focus on pre-crisis liquidity problems in short-term debt-financing markets,1the literature has been largely silent on the liquidity vulnerabilities of the short-term loans that funded nonbank mortgage origination in the pre-crisis period, as well as the liquidity pressures that are typical in mortgage servicing when defaults are high. These vulnerabilities in the mortgage market were also not the focus of regulatory attention in the aftermath of the crisis.Of particular importance, these liquidity vulnerabilities are still present in 2018, and arguably the potential for liquidity issues associated with mortgage servicing is even greaterthan pre-financial crisis. These liquidity issues have become more pressing because the nonbank sector is a larger part of the market than it was pre-crisis, especially for loan ssecuritized in pools with guarantees by Ginnie Mae. As noted in 2015 by the Honorable Ted Tozer, President of Ginnie Mae from 2010 to 2017, there is now considerable stress on Ginnie Mae operations from their nonbank counterparties:

. . . Today almost two thirds of Ginnie Mae guaranteed securities are issued by independent mortgage banks. And independent mortgage bankers are using some of the most sophisticated financial engineering that this industry has ever seen.We are also seeing greater dependence on credit lines, securitization involving multiple players, and more frequent trading of servicing rights and all of these things have created a new and challenging environment for Ginnie Mae. . . . In other words, the risk is a lot higher and business models of our issuers are a lot more complex. Add in sharply higher annual volumes, and these risks are amplified many times over. . . . Also, we have depended on sheer luck. Luck that the economy does not fall into recession and increase mortgage delinquencies.Luck that our independent mortgage bankers remain able to access their lines of credit. And luck that nothing critical falls through the cracks. . .

Varoufakis reviews Adam Tooze's "Crashed"

https://www.yanisvaroufakis.eu/2018/...crash-of-2008/Many economies (e.g. Ireland, South Korea) that were run according to what the global establishment considered best practice (i.e. government and trade surpluses, light regulation of banks and employers) crashed the moment ninety percent of global money flows ceased up. Why? Because the establishments prescription had skilfully left out the crucial truth that the main threat came from the banking system (not the state) and from private (not public) debt. That there were no runs on banks (perhaps with the exception of Northern Rock) meant little: financiers froze up (once called upon to repay unpayable debts, often in excess of their countrys national income) while operating a system whose survival depended on tsunamis of money rushing hither and thither. Meanwhile, American and European politicians, who had grown used to a cosy relationship with the bankers, began to convert a crisis of (super-rich and super-inane) creditors into a crisis of (poor and middle class) debtors, pushing the losses of the former upon the latter also known as socialism for bankers and austerity for the many.

at post #86

Close

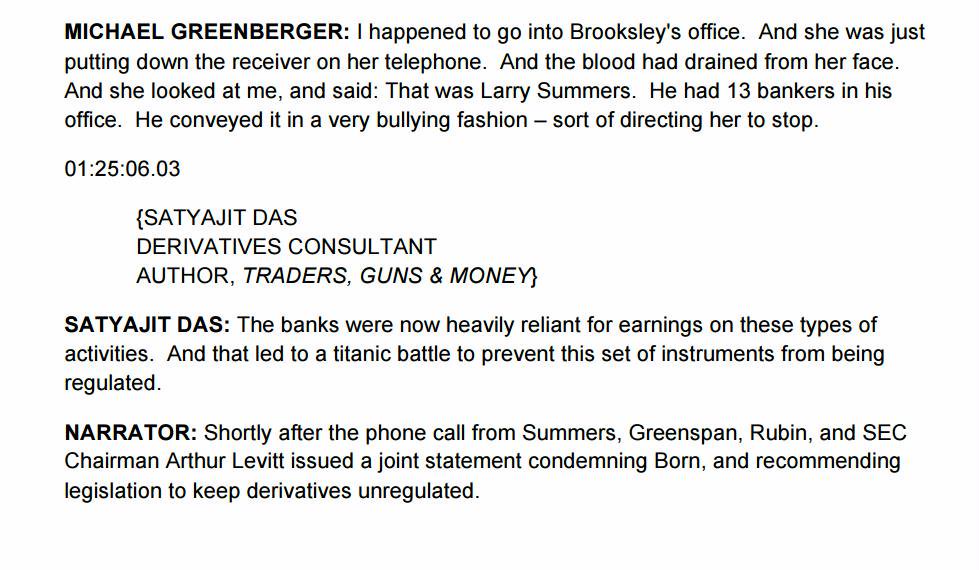

In 1997, the Commodity Futures Trading Commission, a federal agency that regulates options and futures trading, began exploring derivatives regulation. The commission, then led by a lawyer named Brooksley E. Born, invited comments about how best to oversee certain derivatives.

Ms. Born was concerned that unfettered, opaque trading could “threaten our regulated markets or, indeed, our economy without any federal agency knowing about it,” she said in Congressional testimony. She called for greater disclosure of trades and reserves to cushion against losses.

Ms. Born’s views incited fierce opposition from Mr. Greenspan and Robert E. Rubin, the Treasury secretary then. Treasury lawyers concluded that merely discussing new rules threatened the derivatives market. Mr. Greenspan warned that too many rules would damage Wall Street, prompting traders to take their business overseas.

“Greenspan told Brooksley that she essentially didn’t know what she was doing and she’d cause a financial crisis,” said Michael Greenberger, who was a senior director at the commission. “Brooksley was this woman who was not playing tennis with these guys and not having lunch with these guys. There was a little bit of the feeling that this woman was not of Wall Street.”

There are currently 1 users browsing this thread. (0 members and 1 guests)

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote