Faced with the choice between the arduous long-term planning and marketing expense of real-sector investment with single digit returns, the quick (and lower-taxed) capital gains on financial and real estate products offering double-digit returns have lured investors. The main connection to tangible capital formation is negative by diverting new borrowing away from the real sector, as recent studies show (Chakraborty Goldstein and McKinlay 2014).

Industrial companies were turned over to “financial engineers” whose business model was to take their returns in the form of capital gains from stock buyback programs, higher dividend pay-outs, and debt- financed asset takeovers (Hudson 2012, 2015a, 2015b). Charting the ensuing rise of interest and capital gains relative to dividends, and of portfolio income relative to normal cash flow in America’s nonfinancial businesses, Greta Krippner (2005, 182) concludes: “One indication of financialization is the extent to which non-financial firms derive revenues from financial investments as opposed to productive activities.”

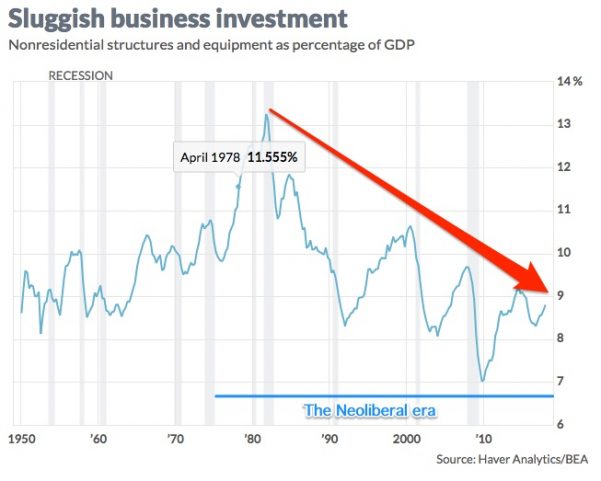

Much as real estate speculators grow rich on inflated land values rather than production, so financialization threatens to undermine long-term growth. Since the 1980s, the major OECD economies have seen rising capital gains divert bank credit and other financial investment away from industrial productivity growth. Engelbert Stockhammer (2004) shows a clear link between financialization and lower fixed capital formation rates.

Reply With Quote

Reply With Quote