Reply With Quote

Reply With Quote

As Katie Martin reports in the FT what dominated the scene was the sheer violence of the market reaction:

On Monday this week (March 13), the most important market in the world went, to use the technical term, completely bananas. Government bonds have a habit of rallying when the going gets tough, which it indisputably did when Silicon Valley Bank imploded. So a jump in US Treasury debt prices off the back of this makes sense. The turmoil prompted nervous investors to look for a safer hidey hole. But there are bond rallies and there are bond rallies. This time, the market reaction in Treasuries was nothing short of apocalyptic. Two-year Treasury notes, the most sensitive instrument in the debt market to the outlook for interest rates, rocketed higher in price. Yields dropped by an eye-popping 0.56 percentage points, having already dropped by 0.31 percentage points the previous Friday. To put Mondays move in context, it represents a bigger shock than in March 2020 not a vintage period for global markets. It was bigger than on any day in the financial crisis in 2008 (ditto). You have to go back to Black Monday of 1987 to find anything more severe.This points both to the scale of the shock and to the uncertainty that rules in the US Treasury markets. Price movements were as extreme as they were in part because the market was thin, with big gaps between bid and ask prices.

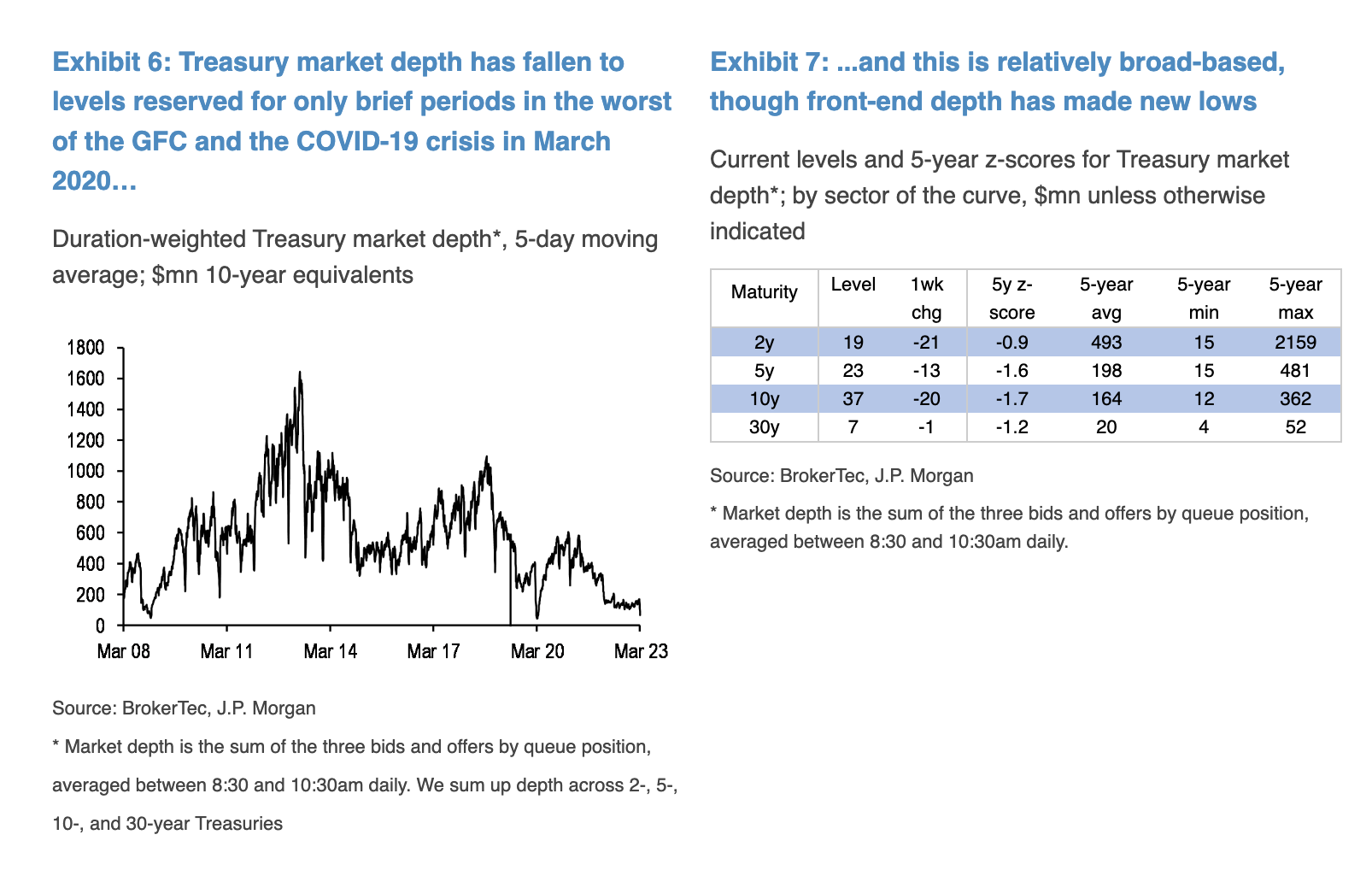

As JP Morgan remarks in a research note:

liquidity conditions (in the Treasury market) remain relatively impaired, indicating that any fundamental or technically-driven flow is likely to exaggerate moves in yields. Indeed, Treasury market depth remains depressed, at levels last seen in the middle of March 2020, during the worst of the COVID-19 crisis (Exhibit 6). Importantly, this decline in liquidity is broad-based in nature, though it is notable that front-end depth has fallen to new lows (Exhibit 7). While this indicates liquidity is impaired, we do not see Treasury market functioning as being compromised to the extent we observed this time three years ago. Indeed, as weve highlighted multiple times in recent months, this illiquidity has been rooted in uncertainty over the path for monetary policy.