Reply With Quote

Reply With Quote

Megan McArdle points a finger at an antequated ling process.

Obviously the lawyers will make hundreds of millions deciding which one of us is right, but you have to mentally draw a line between the original high risk loans secured by the houses and the bonds that were issued with those loans as the underlying collateral. The original loans PLUS AIG's guarantee of repayment is what turned bonds into AAA rated securities. Fanny, Frddie, Goldman, and AIG all made out like bandits till the house of cards came tumbling down...Then, of course, they were all "too big to fail' and the Taxpayers did bail them out and will bail them out again.

Megan McArdle points a finger at an antequated ling process.

http://www.opednews.com/articles/SHO...01003-838.html"The banks simply digitized mortgage les into a privatized system, called the Mortgage Electronic Registry System (or MERS)," he said. "And it did the transfers by trading Excel spreadsheets among the banks and trusts, rather than endorsing the notes as required by their own contracts, by state real estate law and by IRS rules." He stated that 60 million properties are recorded in the name of MERS -- 60% of the mortgages in the USA, and 97% of the loans made between 2005 and 2008.

ibid.MERS is simply an electronic data base. On its website and in assorted court pleadings, it declares that it owns nothing. It was set up that way intentionally so that it would be "bankruptcy-remote," something required by the credit rating agencies in order to turn the mortgages passing through it into highly rated securities that could be sold to investors. MERS not only has no assets; it has no employees. The thousands of people enlisted to sign affidavits on its behalf are merely conduits. The arrangement satisfied the ratings agencies, but it has not satisfied the courts. Increasingly, judges are holding that if MERS owns nothing, it cannot foreclose, and it cannot convey le by assignment so that the trustee for the investors can foreclose. MERS breaks the chain of le so that no one has standing to foreclose. The homes are effectively owned free and clear.

That does not mean the homeowners don't owe money to someone. They do. But the claim for relief is not in "law" (by virtue of an enforceable contract or rule) but in "equity" (a remedy provided just because it is fair), and MERS is not the proper plaintiff. Every MERS case involves a securitization, which means the real parties in interest are a group of investors somewhere; and before the homeowners can be made to pay, the investors have to come forward and prove not only that they are the parties owed the money, but the actual sums they are owed. In some cases they might already have been paid; for example, by insurers on credit default swaps held by the investment pool. The investors are en led to recover in equity only so much as they are actually out of pocket, not the full amount of the original promissory notes, since they were not parties to those notes and there is no way to re-establish the chain of le.

Robo-Signing: Two Class Actions Raise More Troubling Foreclosure Questions

The mortgage foreclosure and robo-signing mess keeps getting messier. And the giant banks that have been caught up in the crisis have plenty of company, including Lender Processing Services and its subsidiary LPS, which plays a huge role in foreclosure process now in high gear across the U.S. LPS describes itself as the nation's "number one provider of mortgage processing services, settlement services and default solutions," working with all the top-50 banks in the country.

To provide its "default solutions," LPS maintains a nationwide network of attorneys who do enormous volumes of foreclosure work. The core of the service LPS provides is a software application that enables its attorneys to communicate with LPS and with LPS's financial ins ution clients. Do ents are uploaded, and sometimes created, in the system and then distributed for signing, often as it turns out, by robo-signers. LPS makes money from its default services work primarily via the various fees it charges attorneys it refers cases -- far more so than from the fees it charges its bank/mortgage servicer clients.

http://www.dailyfinance.com/story/cr...sure/19665854/

I wonder if any politicians (not Repugs, of course. They whine falsely about govt when the real culprit is private, which they want to hide from the bubba dumb s) want to exploit this mess and really punish these predatory, parasitic s bag middlemen (aka lawyers)?

The le insurance mess:

After Foreclosure, a Focus on le Insurance

http://www.nytimes.com/2010/10/09/yo...gewanted=print

So that could put dampen sales of millions of foreclosed homes, and sales of le insurance on those buyers' homes (leaving the supposed le holders/banks paying property taxes and insurance while the houses are in limbo), since who can be sure of who really owns the house.

The Business of America is ing Up Business.

"attorneys general of up to 40 states plan to announce soon a joint investigation into banks' use of flawed foreclosure paperwork.

an announcement could come as early as Tuesday"

http://www.huffingtonpost.com/2010/1...tml?view=print

Again, I seriously think that those financial wizards are all either mentally incompetent or pure s . Not sure which.

There should never be a law that allows digital images have the same force of law as original signatures. Too easily copied.

Foreclosure Fraud For Dummies, 1: The Chains and the Stakes

Posted in Uncategorized by Mike on October 8, 2010

The current wave of foreclosure fraud and the consequences for the economy are difficult to follow. As such, Im going to write a few posts to simplify what is going on so you can follow stories as they unfold. This is very 101 level, and will include a reading list of blog posts and articles at each stage to help provide depth. (Special thanks to Yves Smith and Tom Adams for walking me through much of this.) Lets make three charts of the chains involved in the process. The first is what is currently going on with foreclosure fraud (click through for larger).

As you can see, in judicial review states like Florida the courts require that servicers, or those who administer the bonds that are full of mortgages (securitization, residential mortgage backed securities, RMBS, are all phrases for them), say that they have everything necessary in order to have standing to bring a foreclosure. They need to have the note for a mortgage, which is supposed to be in the trust part of the mortgage backed securities that they administer.

What is breaking down here? In Florida, a judicial review state, it was found that one person was notarizing do ents far faster than anyone could reasonably have. Forged do ents necessary for the foreclosure process like the note were found. A separate court system was set up to resolve these foreclosures faster at the expense of allowing serious challenges to the do ents. Heres Smith on how kangaroo these courts look up close. Heres WaPo on one individual and the nightmare of trying to challenge an invalid foreclosure. Keep him in mind when you hear about deadbeats and whatnot: the current system is designed to make it difficult for anyone to challenge their case.

Meet the robo-signer who kicked it off here at this WaPo story. I almost feel bad for this patsy; the real battle here is between junior and senior tranche holders, and this doofus could end up in jail in order to keep John Paulson rich. After reading about this guy Im asking our elites to take care of their patsies better. (Can we get a Financial Patsy Fordism social contract movement going? If you are going to be a patsy for GMAC, you should be paid enough able to be able to buy GMACs services or something.)

Why would servicers do this? One story would be that the more foreclosures they process, the more fees they get, so there is an incentive to cut as many corners to speed through the process as possible. Hence the term foreclosure mills. You can read more about this from Andy Krolls excellent work for Mother Jones (start here).

Theres another problem though what if servicers are behaving this way because the actual notes arent in the trust? Lets go back to the creation of these instruments.

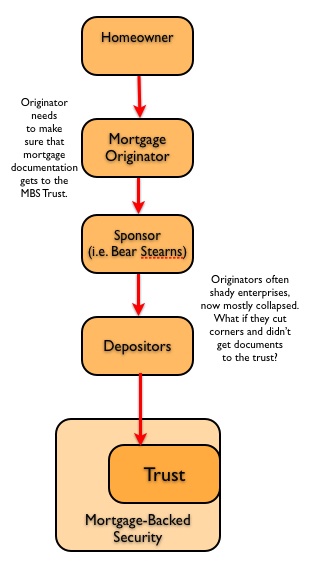

I take a mortgage out at Joes Lending, a mortgage originator. A mortgage consists of two parts. The first is the note, or the IOU, which is the borrowers promise to pay. The second is the mortgage, which is the security, or the lien, or the actual interest.

Joes lending takes the mortgage note to a sponsor to turn these mortgages into a bond. The sponsor was often an investment bank like Bear Sterns. Now that investment bank puts an intermediary in between itself and the trust. This intermediary is usually called a depositor, and sometimes there are several of them in the chain.

Whats the worry here? Well many of these mortgage originators were fly-by-night shops, shady enterprises that collapsed the moment they hit trouble. And many of them cut corners and one of the corners they may have cut would have been to send the note to the trust. Specifically, there is worry that many mortgage originators never sent the notes to the depositors. Originators wanted volume to get fees and may not have done all the paperwork correctly. There are a lot of things that have to end up in the trust when I take out a mortgage, things like the note, le insurance, supporting do ents. But the note is the most important.

Why is this important? Well the trustees usually sign several certificates saying that they have verified all the do entation in these trusts. Many of these trusts are under New York trust law which is particularly clear and strict when it comes to these matters. With this in mind, tackle these three posts by Yves Smith (one two three).

So connect the two together, and you can see why we might have a systemic crisis on our hands:

There are roughly $2.6 trillion dollars in mortgage backed securities. The Wall Street Journal starts to explain how this will be a battle between holders of junior and senior tranches of debt. It also exposes the servicers, which include the four largest banks, to extensive legal liabilities by those who bought these securitizations that were signed off as being properly administered and created.

One result is that this has lead homeowners to reasonably demand to see the proper do entation before they and their families are put out on the street. Read Ryan Grim and Shahien Nasiripour from June, Who Owns Your Mortgage? Produce The Note Movement Helps Stall Foreclosures.

Katie Porter is an expert who has done extensive research into this area and often blogs about it at credit slips. See the blog posts: How to Find the Owner of Your Mortgage and Produce the (Bogus?) Paper. Porter found that this was extensive in her research, see Misbehavior and Mistake in Bankruptcy Mortgage Claims (A majority of mortgage claims are missing one or more of the required pieces of do entation for a bankruptcy claims. Fees and charges on claims often are poorly identified and do not appear to be reasonable. The bankruptcy data reinforce concerns about the overall reliability of the mortgage service industry to charge homeowners only the correct and legal amount of the debt and to comply with applicable consumer protection laws). By rushing the process, unreasonable and excessive foreclosure fees can get applied to homeowners when there may not even be the proper do entation to have the standing to bring foreclosure at all.

So keep these frameworks in mind when you see the debate unfold in the next weeks. It is a problem of systemic risk, and it is a problem for the currently cratered securitization market. It will need to be addressed, the sooner the better. But how?

I read an article, WaPo/Perlstein?, that still implies that all responsibility is on the home owners, with something like "no matter what the screw ups are on the lenders'/servicers' side, the homeowners are still delinquent", with no mention that the lenders in the housing bubble were, as is the case in 90% of mortgage fraud, the guilty party for lending to borrowers they the lenders didn't prove credible borrower ability to sustain the payments.

Nobody forced the lenders to write ty loans, just like CRA didn't force lenders to write sub-prime/teaser mortgages for poor blacks/browns, clearly proven by the fact the the govt can't now get to lenders to modify mortgage terms.

Go free market! Less regulation will help protect consumers!

What can the courts do when presented with fraudulent do ent? When the proof is shown of fraud, then those responsible need their asses kicked so hard, they can never do it again. No amount of regulation will help is the justice system is asleep at the wheel as well.

Here's Cantor today trashing the irresponsible borrowers, while saying nothing about the lenders:

"you have 10 percent, if that, of the population who are now in a foreclosure situation or in a mortgage that they have been unable to meet the obligations… Now, come on, people have to take responsibility for themselves."

http://thinkprogress.org/2010/10/10/...defends-banks/

As is always the case with Repugs/conservatives, esp our beloved WC and CC, the corps/capitalists/Haves are innocent, beyond reproach, and the HaveNots are criminals to bear full responsibility.

http://www.nakedcapitalism.com/2010/...re-crisis.htmlDebunking Banks’ “Procedural Problems” Defense on the Foreclosure Crisis

As more and more problems with foreclosures and borrower horror stories are coming to light, it isn’t hard to notice that banks are still gamely sticking with the pitch that the failings are technical and procedural even as the breadth of their response and the official reaction says otherwise. Suspending all foreclosures in the US, as Bank of America did today, is a very significant move. And the pressure appears to be escalating, as a multi-state effort is close to going live.

Per Bloomberg:

Attorneys general in about 40 states may announce by next week a joint investigation into potentially faulty foreclosures at the largest banks and mortgage firms, according to a person with direct knowledge of the matter.The Financial Times gives us Bank of America’s gloss on this shoddy situation:

State attorneys general led by Iowa’s Tom Miller are in talks that may lead to the announcement of a coordinated probe as soon as Oct. 12, said the person, who asked not to be named because an agreement wasn’t completed. The number of states may change because several are deciding whether to join, the person said. New Mexico Attorney General Gary King said yesterday in a statement that his state will join a multi-state effort.

Banks have downplayed the problem by saying it is a mere technicality, adding that they are only foreclosing on homeowners who are months behind on their mortgage payments. BofA reiterated that position on Friday, saying:Yves here. Although we have chronicled the affidavit improprieties, we’ve kept our focus on the fact that these abuses are symptoms of much bigger, and we believe pervasive, problems with the securitizations. But in trying to give the big picture, we may have played into the bank narrative of minimizing the importance of the affidavit issue. Reader ella in comments provided a reminder:

“Our ongoing assessment shows the basis for foreclosure decisions is accurate.”

An affidavit is a legal do ent which can subs ute for live witness testimony in court. All testimony in court is governed by the rules of evidence or by statute. All testimony requires that the witness swears to tell the truth, is competent and has personal knowledge of the facts they are testifying about. An affidavit is no different, in most if not all jurisdictions; the affiant swears to tell the truth by being placed under oath by the notary, the affiant states in the affidavit that they were sworn, are competent and that they have personal knowledge of the facts in the affidavit. The notary attests to the oath of the affiant and that the affiant is who he claims to be.

If a witness lies in court or in an affidavit then they could be charged with perjury. Perjury is lying to the court.

The affidavit issue is being portrayed in the MSM at a paperwork problem. Lying to the court is not a paperwork problem. Attorneys are prohibited from making a material misrepresentation to the court of fact or law. Further, attorneys in most jurisdictions have an affirmative duty to report known perjury by their clients to the court.

The problem with the affidavits is perjury on behalf of the affiants and possibly the notaries depending on the notaries’ knowledge that the affiants had not reviewed the files, the promissory notes, the mortgages, or the records of default.

Further, you can reasonably argue that the en ies pursuing foreclosure (banks or servicers) have perpetrated a fraud on the court by submitting perjured affidavits. If the attorneys representing the en ies have knowledge of the fraud or are preparing questionable do ents then they may also be involved and subject to penalties.

At the heart of any trial or hearing is the determination of the truth of the matter. It is the very purpose of the rules of evidence and what law and fact is presented to the court. If the affiants lied, as it appears, then the truth of whether they owned the note and held the mortgage and the borrower was in default is at issue. Courts, Attorneys General, and bar associations need to serious consider actions that will assure compliance with the rule of law.

This country cannot stand as a democracy if there is one set of law for the banks, corps, elites and another set of law for the rest of us. Perjury and fraud on the court is very serious matter. It is not a mere paperwork problem.

Here's more the CRA lie:

Conservatives Push Absurd Lie that Wall Street Hustlers Were Innocent Victims ... of Poor People

Perhaps the most pernicious right-wing lie of late is that the Wall Street hustlers who came close to bringing the global economy to its knees in 2008 were just innocent victims of government-sponsored programs that forced them to lower lending standards in a misguided effort to increase home ownership among the poor (read: dark-skinned).

http://www.alternet.org/module/printversion/148454

===========

And like the shills here for warming deniers, the same shills here immediately, in 2008, blamed the Dems, Freddie, Fannie, CRA for screwing up the lenders and mortgages. Total and complete lies.

Obama has said no moratorium is necessary, stressing, like the banks, the "valid basis" for foreclosure instead of fraud and contempt for the rule of law on the part of the banks.

If borrowers cheat on their paperwork they face jail. If banks do it the President of the USA stands behind them and stresses the "valid basis" of their fraudulent acts.

The sense of priorities is astonishing. Axelrod repeatedly stresses the need to get “this” resolved quickly. Notice the refusal to use accurate and honest language: at best, these are improprieties, but the more accurate word is fraud.

Bank Disinformation II: Banks Attacking Rule of Law Frontally

Readers may argue I’m reading more of a bank PR role in a page one Wall Street Journal story than is warranted. However, even the Columbia Journalism Review took notice of the Journal’s scanty reporting on the foreclosure crisis, a mounting series of problems that is deservedly damaging to the banking industry’s image and bottom line. Now we have the Murdoch paper feature a remarkably one sided story on foreclosures. That looks to be no accident.

The story, “Courts Add To Foreclosure Delay” is utterly one sided. Having a judicial process for making foreclosures, as is required in 23 states, is bad for you….because it is preventing the housing market from bottoming. This argument is the polar opposite, by the way, of the Administration’s lame defense of its HAMP mod program.

Readers may recall that HAMP for the most part merely delayed foreclosures of participating homeowners for a few months, allowing banks to extract a few more payments from stressed borrowers and extract some incentive fees. Team Obama contended that was really a good thing, a feature, not a bug. The housing market was weak; better to have foreclosure properties dribble out on the market to prevent overshoot on the downside. So it seems that bank defenders will spin the delay issue whatever way they need at any point in time to flatter the banks.

The author also leads with an exaggerated claim up front:

One comparison widely cited: In California, where judges don’t handle foreclosures, the housing market appears to have hit bottom a year ago and has been bouncing back. In Florida, where foreclosures go through the court system, prices keep falling, and foreclosure inventory continues to rise.Correlation is not causation, and indeed, the author backpedals, but it’s a full 13 paragraphs later:

The judicial process isn’t the only determining factor. California’s economy is more diverse than Florida’s and real estate, long term, has always been a stronger bet in California, which explains why buyers would pounce once prices declined.The article attributes differences in foreclosure times solely to the judicial versus non-judicial issue. Yet it has repeatedly been reported that banks themselves are failing to foreclose on severely delinquent borrowers. Indeed, the “deadbeat borrower” reaction comes up repeatedly whenever we talk about people fighting foreclosures. In fact, relatively few people who can’t afford their homes fight; most are beating back a bank motion to break a bankruptcy stay or believe they are the victim of servicing errors; in Florida, some were partway through getting mods, yet the servicer failed to call off the foreclosure mill. The banks aren’t about to release the data, but a fair bit of the lengthening of time to foreclosure is due to the banks’ choice: they keep the borrower in place so that they are liable for the real estate taxes. If a bank has a lot of real estate already in a certain city or area, it’s going to have trouble moving inventory, so it sees delaying foreclosure as a way to save holding costs.

There is also not a single acknowledgment in the article that affidavits submitted were improper. Look how timid the Journal’s formulation is: “alleged irregularities in foreclosure do ents submitted by the banks.” The banks have ADMITTED the affidavits were fraudulent, prepared by people who had no direct knowledge. This isn’t an “allegation”; these are admissions by bank employees in multiple depositions.

The article focuses strictly on the same theme of the Axelrod Face the Press remarks on Sunday: delay is bad for the economy, and gives as little mention as possible to the dead body in the room, that the “do entation” problems are severe and not fixable in any simple fashion.

That isn’t to say that some of the issues and data in this article aren’t worth exploring. But this piece was not an inquiry; it’s a badly skewed account, but the framing and the heavy use of data provides effective camouflage.

On another front, we had a pretty lame sighting over the weekend, the president of MERS, Mortgage Electronic Registry System, trying to defend his firm’s activities. We’ve avoided talking much about MERS, simply because it is a secondary problem in the foreclosure mess. The big failing of the securitization industry was not conveying the borrower IOU (the note) correctly to the securitization trust. In 45 of 50 states, it’s no tickie, no laundry: if you don’t own the note, you can’t foreclose. The mortgage (aka a deed of trust) is an “accessory” to the note in those states.

Some statements made in a Q&A released in connection the the president’s remarks are patently untrue, as in they have been repeatedly contradicted by sworn testimony by MERS employees. For instance:

1) MERS holds legal le to a mortgage as an agent for the owner of the loanThis is utter baloney. MERS has no legal relationship to the note-holder. The owner of a loan (in the MERS context) will always be a trust. Per Max Gardner, a Federal bankruptcy attorney:

2) MERS can become the holder of the promissory note when the owner of the loan chooses to make MERS the holder of the note with the right to enforce if the mortgage loan goes into default.

The Trust is NOT a member of MERS by a bi-lateral or tri-lateral agreement. The Trust cannot be a member of MERS per the MERS By-Laws. The Trust has never signed any do ent or filed any do ent that appoints MERS to execute any do ents for the Trust. You simply cannot have a silent or unauthorized “agent” or “nominee” for a NY or Delaware Trust without a specific designation and appointment by the Trust…..The mortgage note is never transferred to MERS.There is more from the Q&A that is false:

Claims that MERS disrupts or creates a defect in the mortgage or deed of trust are not supported by fact or legal precedents….MERS does not remove, omit, or otherwise fail to report land ownership information from public records.Yves here. Ahem. This is misleading. There is no public record of the transfers from the originator to the trust (assuming that was done correctly).

MERS also falsely insists it increases transparency:

MERS was created to provide clarity, transparency and efficiency by tracking the changes in servicing rights and beneficial ownership interests. It was not created to enable faster securitization.Um, MERS was create to save recording fees. And transparent? Absolutely not. Only MERS members, which are basically banks and servicers, can access the service. And it appears any MERS member can assign a mortgage. Moreover, from what I can infer, MERS is lacking in the sorts of checks you’d expect in a registry of this importance (requirement of approval or confirmation by a second party of a records change; audit trails, etc).

Although the MERS effort at image-burnishing is a side show, it’s still worth noting that they can’t even keep their own story straight. And MERS is hardly alone in that regard.

The foreclosure fraud confirms the hsitory that mortgage fraud has been 90% of the time by the lenders, not the borrowers.

Isn't it fraud to knowingly take on responsibilities you cannot make good on? Not everyone losing houses lost income.

Now I'm not supporting the banks here. I think those doing bad business practices should own up to it, and go bankrupt if necessary. No bailout. However, with you, it's always the big guys fault. Never the little guy.

What history are you talking about, b_d?

The last ten years? The last 100?

Irresponsible borrowers aren't responsible for banks faking their foreclosure paperwork.

I agree. As I have pointed out in past posts, I agree with that point. To me, those responsible need to be locked up!

Borrowers were NOT vetted thoroughly by lenders who wanted to write (sub-prime, teaser, balloon mortgages, pocket their fees, and sell the mortgage into the MBS hole.

the power (knowledge) imbalance between a probably first-time mortgage borrower and a lender armed with accountants, lawyers, and the experience Ks or Ms of mortgages is exactly how the LENDers like it.

Ever hear of lenders accepting borrowers on "stated income" and "liar's loans"? It was rampant in the most bubbly regions. The lenders had many way to block incapable borrowers (like applying federal law, 2 years of bank statement, 2 years of income tax statements, etc, etc), but they simply didn't. They were flipping mortgages for the fees and flipping mortgages they wouldn't have to service.

Last edited by boutons_deux; 10-11-2010 at 09:38 AM.

There are currently 1 users browsing this thread. (0 members and 1 guests)

Posting Permissions

Posting Permissions